TABLE OF CONTENTS

1. CANADA NEEDS TO CONQUER COVID TO GET MOVING AGAIN

Almost two months into 2021, and it feels like we’re stuck in 2020.

But past Groundhog Day and into the long shadow of COVID-19’s dark winter, the horizon holds hope of getting vaccines into arms and Canadians moving again.

For the 2021 rental market, Canadians moving again will finally put 2020 in the rearview mirror.

So, what’s ahead this year for the Canadian rental market?

Rentals.ca and Bullpen Research & Consulting predict asking rents could go even lower in the first four to five months of 2021, but will rebound up 3 per cent nationwide by the end of the year. Asking rents are also forecast to increase in Toronto (+4 per cent), Montreal (+6 per cent), Vancouver (+3 per cent), while staying flat in Calgary.

“In many markets, rents have dropped to the point where tenants can lease an apartment with an additional bedroom for the same rent as they were paying last year,” says Matt Danison, CEO of Rentals.ca.

“For the first time in decades, tenants have a lot of negotiating power, as listings increased significantly in 2020,” says Ben Myers, president of Bullpen Research & Consulting. “Many tenants are no longer constrained by their commute, and seeking cheap accommodations, or more space.”

For this report, Rentals.ca gathered the perspectives and insights of experts across Canada including Canada Mortgage and Housing Corporation economists and analysts, housing data analysts, investors, and rental market specialists.

Their consensus for the 2021 rental market?

Cautious optimism, continued resilience in working through the pandemic and — hope for better collaboration among renters, landlords and governing authorities.

More specifically, many believe:

- Working from home will stick around post-pandemic

- Supply will continue to outpace demand for the first half of the year

- Asking rents — especially in the larger metropolitan areas — will continue to fall, but make a turn possibly before summer

- Incentives will continue this year to entice prospective tenants

- Vacancy rates will remain high for more expensive units but will be tight on the lower end of the market

- Smaller cities surrounding major metropolitan areas will continue to thrive — especially near Toronto

- Virtual tours and digital transactions have become a bigger thing during the pandemic, and most see these becoming a more common part of the renting process

The rental market as most all aspects of the economy depend on dispensing vaccines and conquering COVID-19.

Most hope by Canada Day (Montreal’s Moving Day), the border will be open, immigrants will come again to Canada, travel and tourism will be back, the unemployment rate will decline, and students will prepare to return to student apartments for fall classes.

The Rental Market Survey, released in late January by the Canada Mortgage and Housing Corporation‘s (CMHC) reported the overall vacancy rate in Canada increased to 3.2 per cent in October 2020 up from 2 per cent in October 2019.

“The economic impact of the pandemic has significantly reduced rental demand,” says Bob Dugan, CMHC’s chief economist. “Lower international migration, fewer student renters and weaker employment conditions led to weaker inflows of new renters. While vacancy rates increased in many centres, we continue to see a need for more rental supply to ensure access to affordable housing.”

CMHC conducts the Rental Market Survey annually in October to gauge how socio-economic conditions, demographic trends and other factors impact Canada’s rental markets. The survey is based on purpose-built structures with three or more rental units in urban areas with populations of more than 10,000. The survey includes all rentals including occupied units.

2. WHAT RENTERS WANT

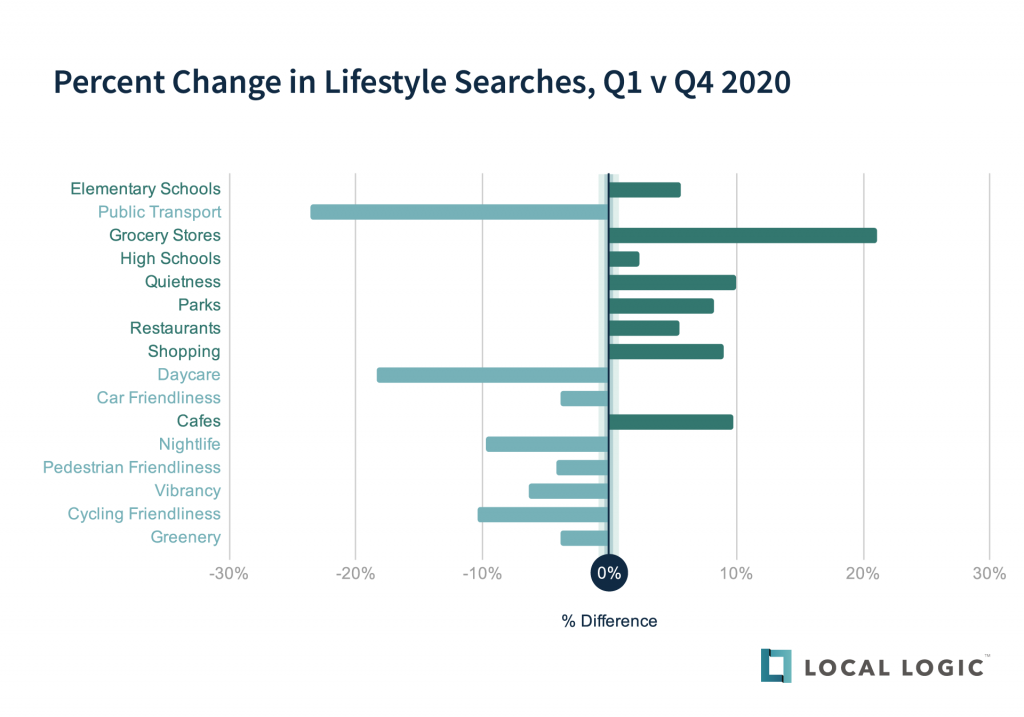

To capture changes in renters’ lifestyle preferences as a result of the pandemic, Local Logic of Montreal compared the first quarter and fourth quarter of 2020.

Two categories showing major differences were public transport — down 24 per cent in interactions by renters from Q1 to Q4 and groceries — up 21 per cent in interactions.

“COVID-19 had clear effects on renters’ preferences this year,” says Guy Tsror, data scientist for Local Logic. “Proximity to grocery stores and parks shot up in Canada — 21 per cent and 8 per cent respectively. On the other hand, we saw a sharp decrease in interest in nearby public transport, going down 24 per cent by Q4, compared to Q1 of 2020.”

But Tsror believes less interest in living near public transit will be “a short-lived trend that will slowly recover as vaccinations become a reality, as it is still in the top three most desired location characteristics, in spite of the decrease.”

Other areas that showed movement were increased interest in quietness and park access — between 8 per cent and 10 per cent increase. Interest in day care went down 18 per cent, possibly due to many parents now working from home.

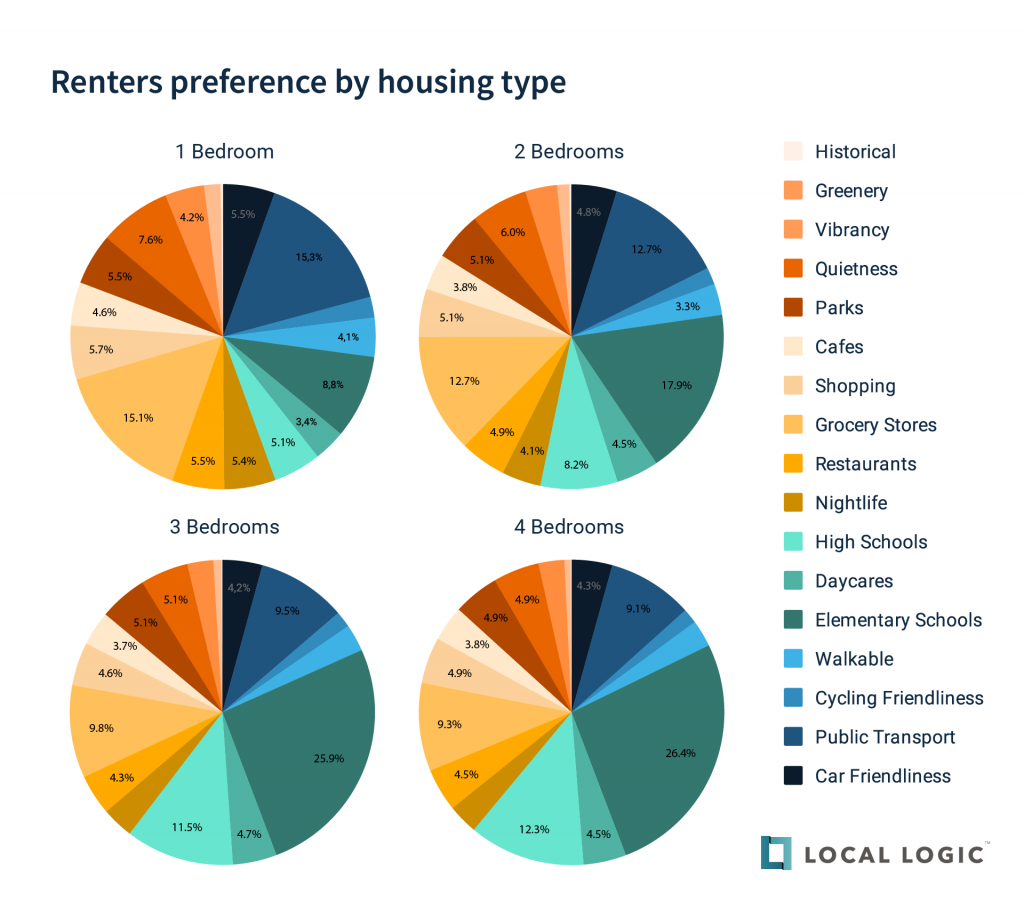

Schools still lead all other categories for renters’ preferences. This is especially true for renters (most likely families) looking for larger units. Grocery stores, as well as public transport, are more important to one-bedroom unit renters, accounting for a larger portion of their interactions.

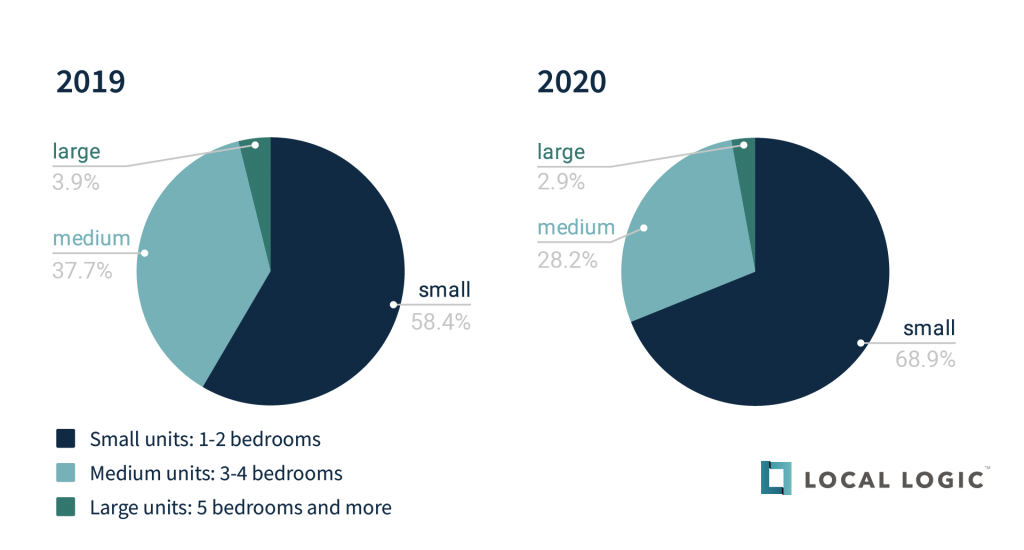

Year over year, smaller units made up 68.9 per cent of the rental market in Canada in 2020 (an 18 per cent increase compared to 2019), most likely due to the flow of short-term rentals and the student-occupied listings added to the market.

Year over year, smaller units made up 68.9 per cent of the rental market in Canada in 2020 (an 18 per cent increase compared to 2019), most likely due to the flow of short-term rentals and the student-occupied listings added to the market.

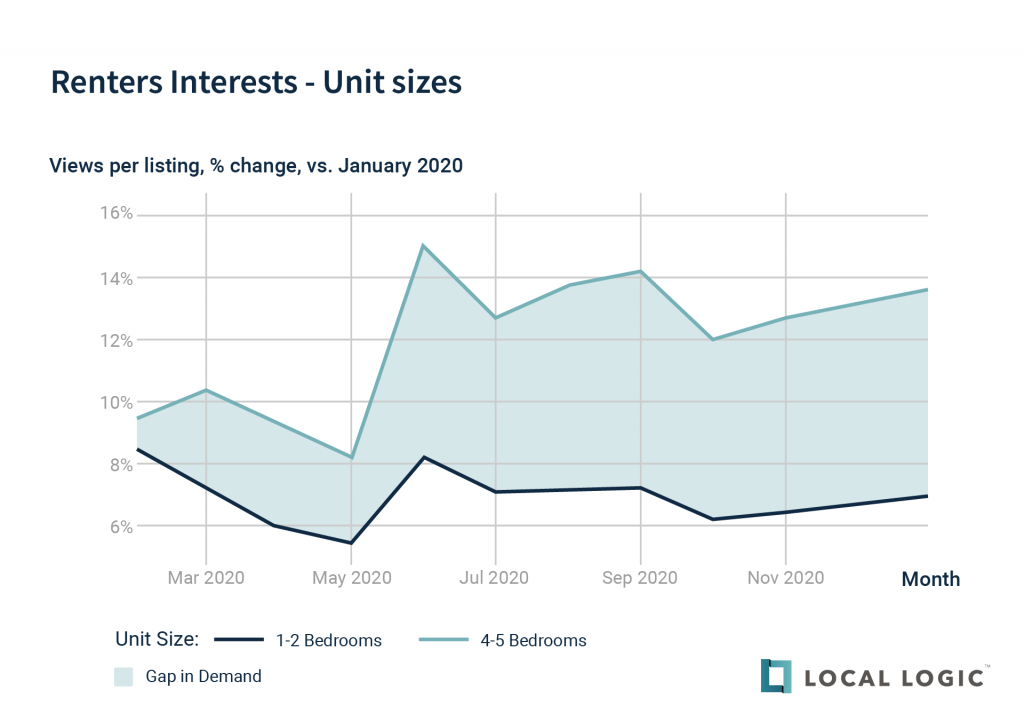

While the inventory leaned heavily toward smaller units, larger units were more in demand, he says. Smaller units were less frequently visited by searchers in 2020, compared to the year before, while bigger, three- to five-bedroom units saw an increase in views per listing. Four-bedroom units saw one of the largest changes — a 53.9 per cent rise in views per listing year over year.

Demand went down for all units between March and May and started rising after, but larger units finished the year on top. Compared to January 2020, demand rates by the end of the year, for four- and five-bedroom units was up 13 per cent and 47 per cent respectively, while demand for smaller one- and two- bedroom units was down between 26 per cent and 15 per cent respectively.

In Toronto, the viewing rate for smaller units has remained generally unchanged between Q1 and Q4 (between -0.6 per cent and 0.78 per cent change), while larger units have seen a growing increase: four-bedroom units and three-bedroom units saw 23.6 per cent and 13 per cent increases, respectively. Inventory numbers in Toronto went up as well, with 104 per cent more one-bedroom units in Q4 compared to Q1, but only 41 per cent more three-bedroom listings.

Tsror says in the cities surrounding Toronto, “demand for rental units of any size went up, suggesting renters want to live outside of the core city centre, now that they can work from home without commuting each day.”

In Montreal, demand for rentals decreased between Q1 and Q4. One-bedroom units were viewed almost 52 per cent fewer times in Q4 compared to Q1, marking the biggest drop, while four-bedroom units saw a decrease in views as well, but slightly lower, at 27 per cent fewer than Q1, he says.

Local Logic products are used on approximately 80 per cent of the real estate portals across Canada.

3. WHERE RENTERS WANT TO LIVE

Rental demand was strongest in the secondary and tertiary markets in 2020 as COVID-19 took hold of the country.

“As many cities — especially those in primary markets — experienced a rapid decrease in rental demand this year, numerous cities in secondary and tertiary markets have continued to thrive throughout the pandemic,” says Jason Leonard, co-founder and president of Rentsync, a provider of multifamily marketing software and services.

The work-from-home trend has strengthened because of the pandemic causing many employees to leave downtown cores of major metropolitan areas searching in smaller cities for more affordable rentals with more space to live and work.

“Many renters are taking advantage of this opportunity to find housing in areas that accommodate this lifestyle over proximity to work and transit, while also keeping their families safe and healthy,” Leonard says.

Three secondary cities in British Columbia experienced high rental demand year over year: Richmond, up 45 per cent; Nanimao, up 26 per cent and Victoria, up 14 per cent, according to Rentsync data. (For an overview of the rental demand trends across Canadian cities, see the latest Rentsync National Rental Demand Report, which provides data-backed analysis using aggregate ILS data from over 20 rental listing sites).

The two tertiary markets with the highest rental demand in 2020 are Sudbury, ON, up 17 per cent and Saskatoon, SK, up 11 per cent, according to Rentsync.

Other markets with strong rental demand in 2020 include St. John’s, NL, up 21 per cent; Coquitlam, BC, up 9 per cent and Kingston, ON, up 5 per cent. Demand could continue to be strong in these three cities this year given early indicators of month-over-month growth. January data shows St. John’s, NL up 30 per cent; Coquitlam, BC, up 7 per cent, and Kingston, ON up 23 per cent.

Leonard does not see the work-from-home phenomenon going away any time soon.

“As renters have left their small apartments and fled to more spacious secondary markets in the second half of 2020,” he says, “residents are just finding their roots in these new cities, and are enjoying a more spacious living and working environment.”

But he does see renters coming back to primary markets such as Toronto once the border reopens, travel restrictions are lifted, and students come back to campuses and look for student housing.

This is especially true as rental rates continue to decrease in major markets. “This shift will reach a breaking point,” Leonard says, “and interest in primary markets will once again reappear.”

Another trend from the pandemic that will stick, according to Leonard, is the continued digital influence on rental transactions. From listing services to virtual tours of apartments, both tenants and landlords are relying more on digital solutions for the best rental experience.

“As borders open and temporary residents look to urban areas for rentals,” he says “they, too, will require more digital solutions to help make their rental experience as smooth as possible.”

4. WHAT’S AHEAD FOR THE REST OF 2021

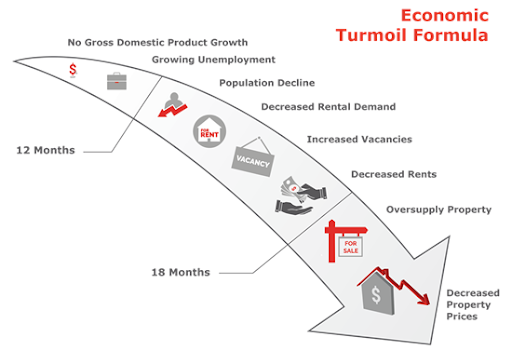

Rents will continue to decrease, applying the Real Estate Investment Network’s (REIN) Economic Turmoil Formula generally — not including specific cities or neighbourhoods — says Jennifer Hunt, vice president of research for REIN and co-founder and CEO of Top Deck Group, which acquires underperforming multi-family apartment buildings.

This formula shows the correlation of key drivers (economic fundamentals such as economic health (GDP), employment (jobs), and population (immigration)) and how they drive rental and property markets. Rentals and property data are lagging indicators. As a general rule, rental markets are impacted 13 months after an economic event, while property prices lag even further and materialize about two years later. (Graphic courtesy of REIN)

Given economic activity has declined at unprecedented levels due to the pandemic, jobs lost, and borders closed affecting immigration, these three key economic fundamentals make the REIN formula a reality for Canada, says Hunt.

Government policies such as – fiscal stimulus (think Canada Emergency Response Benefit (CERB); Canada Emergency Wage Subsidy (CEWS); and Canada Emergency Business Account (CEBA) and monetary policy (think Bank of Canada interest rates at all-time lows), are slowing the impact of these recent declines; serving as a life jacket buoying the economy.

Hunt says many economists suggest these government supports and money will be here for some time, but not indefinitely. With the second pandemic-induced recession upon us, the life jacket may be insufficient to fully float the economy through the full recovery.

There are many nuances to these pandemic recessions, she says. For example, lower-wage service jobs were hardest hit. While less likely to own property, employees in these jobs are more likely to rent. Market influencers such as policies, vaccination rates, ability for businesses to open, will either accelerate or further stagnate Canada’s economic recovery. This will in time be reflected in the rental and housing markets.

“So, to stabilize rents we need to stabilize the economy,” Hunt says, “especially in the hardest hit sectors.

She says to expect bad debt to emerge referring to a comment from Benjamin Tal, deputy chief economist for Canadian Imperial Bank of Commerce (CIBC): ‘Bad debt will come eventually, but it will be a very slow process.’

Supply and demand will change, she believes, “ebbing and flowing as demographic shifts emerge as trends in the foreground or subside into the background.”

As examples, she points to rental demand decreasing because of students not returning to campuses, of immigration being halted, and the emotional fear of moving during the pandemic. On the other hand, more people are moving because of job losses/reduced income, the work-from-home phenomenon and/ relationships ending.

Hunt sees the trend of moving away from downtowns to less expensive markets for more space continuing for a time, but “there again are nuances.”

The transition, particularly of older millennials to “hipsterbias and exurbs” was underway pre-pandemic. (Many older millennials as they have families want more home and property for less money in the suburbs and exurbs where they can now find good restaurants, and other entertainment opportunities they had in downtown metro areas).

Hunt says these trends are accelerated because of COVID-19. Besides affordability and growing families, people want more internal and external space for health reasons, and because of the shift to working from home.

The work-from-home trend accelerated by COVID-19 will continue after the pandemic is over, Hunt believes, “but it will be tempered by a desire to resume pre-pandemic ‘normalcy,’ and by the benefits of collaborating in person on occasion. Where working remotely makes sense, it will continue to expand.”

She says most studies show the economic benefits of working from home to both corporate bottom lines and to employees’ living budgets.

But she says there are indications younger millennials are moving into downtown cores. With unprecedented low rents and vacancies, this younger cohort – without attachments, children, longer-term careers – are seeing the opportunity to move into previously unattainable homes. In many downtown areas, it has been a renters’ market with landlords offering incentives such as a month of free rent, free parking and cash, she says.

Another problem Hunt identifies as hurting the rental market besides the pandemic is rental housing is a low margin business.

Many landlords have had to manage rising costs — insurance alone is upward of a 400 per cent increase – against the backdrop of restrictions like rent controls – which vary, but on the upper end are about 2 per cent per year. Layer on even more pandemic-related restrictions, such as policies prohibiting any rental increases or evictions, and individual investors are stepping away from the market.

Fewer rental housing providers means fewer rentals which exacerbates the pre-pandemic supply crisis. “This supply crisis has not been resolved; it’s a foundational issue”, says Hunt, “it’s just not making the headlines during this pandemic, but it is a challenge that will continue to impact rents in the long run, based on supply-demand economics.”

With conservatively more than 60 per cent of Canada’s rental properties owned by independent investors, according to CMHC and other experts, a lot of rental housing providers deciding to get out of the business would accelerate the rental housing supply crisis.

What’s needed?

“Practical solutions protecting rental stock by way of its operators – the majority of which are mom-and-pop-run small businesses operating on tiny margins, in a highly regulated sector,” says Hunt.

5. PANDEMIC PUSHES PROPTECH TO THE FOREFRONT

“The pandemic has awakened the majority of landlords and property managers alike,” says Jonathan Margel, CEO and co-founder of Building Stack in Montreal. “Proptech is more important than ever and here to stay.”

There are many inefficiencies the average management operation faces each day, he says, and suggests property managers and landlords align with a multi-dimensional platform to help throughout the tenant lifecycle.

Margel says the pandemic has caused an urgency for landlords to adopt proptech to efficiently manage their day-to-day operations, to keep tenants and staff safe, and to “provide the best possible service to ultimately remain competitive to attract prospects.

“The days of face-to-face communication in a rental office to complain about a leaky faucet are over,” he says. “The days of paying your rent by cash or cheques are also dwindling.”

Margel says landlords and property managers need to adopt the right tenant portal, go ‘digital’ for work order management, online rent payments, and in many other ways to stay relevant.

“I find it very unlikely most vacancies will get filled without these types of offerings in today’s new reality,” he says.

One trend Margel sees coming out of the pandemic and becoming more competitive in 2021 is more automation in rental buildings.

For example, he points to “the need for better solutions to receive, store and distribute packages to tenants.”

Better entry systems, storage lockers, package rooms and door lock automation will continue to be adopted by more and more landlords in both new construction as well as retrofitting older properties in 2021, Margel says.

6. TORONTO

Myers of Bullpen Research & Consulting believes all the new supply scheduled for completion in 2021 in Toronto and the Greater Toronto Area (GTA) will only exacerbate the rent price decline early in the year.

“My expectation is that average rental rates will continue to decline for the first four to five months of the year,” he says, “But they will pick up in the second half of the year as vaccinations increase and COVID numbers decline.”

Myers believes the biggest issue in Toronto is the downtown condo market, “where tenants have less incentive to lease because offices are not open, and most of the major attractions and neighbourhood amenities are closed.”

“A major decline in COVID numbers will be the only thing that reverses this trend,” he adds.

He also sees the trend continuing of renters moving to cheaper suburban suites and avoiding the “tall towers with long elevator rides.

“Some of these renters are taking advantage of low interest rates to buy condos in the suburbs, with November resale activity in the ‘905’ area up 23 per cent annually, and the average resale price up 5 per cent annually,” he says. “If those numbers continue to rise, it will make downtown more attractive by comparison.”

With the second lockdown underway, he says, three- and four-storey walk-up apartments will continue to attract a premium price, while tenants will continue to look more for homes with private outdoor spaces, terraces, large balconies, backyards or shared courtyards.

Expensive properties with lots of amenities — that are not open — will continue to be hard to fill, Myers says, so, “expect even larger incentives to attract tenants — anything but a rent discount.”

Myers says the Toronto Census Metropolitan Area has the highest share of adults living with their parents than any other metro in Canada.

“At some point the rent declines will be enough to entice them to jump into the market,” he says. “Tenants are going to try to time the bottom of the market, and that bottom may come as soon as March.”

Tony Irwin, president and CEO of the Federation of Rental-housing Providers of Ontario (FRPO), is reluctant to predict what rents will do in Toronto in 2021, but he sees lower rents and higher vacancy rates as “temporary.”

He says rents were down 3 per cent to 6 per cent in Toronto and 2 per cent in Ontario in the last quarter of 2020. Irwin said the vacancy rate in downtown Toronto is around 4 percent, up from 1 percent at the beginning of 2020.

Some landlords are offering incentives in certain markets to get units rented, especially where vacancies have spiked.

The head of the organization of more than 2,200 landlords is optimistic the trend will turn, and the economy will get better, but as to when, “I don’t know the answer to that.”

He says the recovery will happen as immigration, students — international and Canadian — and more jobs come back, and the border is reopened.

Until then, FRPO has developed a guideline of “best practices” for its membership during and past the pandemic. Early on, FRPO formed an emergency ad hoc committee of professionals, property managers and experts which devised guidelines for landlords, tenants and employees called “Preparing for the Future: Guidelines for Managing/Operating a Multi-res Property in a Post-COVID-19 World.”

The document for FRPO members touches all aspects of running a multi-residential property from setting up cleaning protocols to keeping residents safe.

Among the many thoughts, precautions and suggestions are: how to handle moving, maintenance, leasing, virtual leasing, how to promote safety when using amenities such as kitchens, gyms, media rooms, pools and children’s play areas, and how to deal with guests, deliveries and contractors.

All topics in the extensive and expansive document are filtered through a four-tiered modified COVID-19 risk mitigation model.

Irwin says the committee is still meeting, and he believes some of the measures such as cleaning protocols and virtual leasing will become permanent.

FRPO also offers the latest on COVID-19 resources and information for the rental housing industry.

Beyond the pandemic, Irwin believes that while COVID-19 has overshadowed Toronto’s housing shortage crisis, “the problem hasn’t gone away; it’s just delayed.”

He points to a FRPO-authorized Urbanation report — ‘Revisiting the Supply Gap & Opportunities for Development’ — published last year showing a shortage of 20,000 residential units a year for 10 years.

“While we might go back to the way things were at some point,” Irwin said, “We will still have a supply crisis.”

The study identified about 950 infill or ‘unicorn’ sites where about 176,000 units could be built in the Toronto/Hamilton corridor. The number of units is now closer to 161,000 because 8 per cent of them have a current development application. Infill or unicorn sites are already purchased and zoned — there’s simply room and an opportunity to add more.

He says turning “some of these unicorn sites into shovels in the ground” is a next step in helping solve the supply crisis in the next 10 years.

Besides NIMBYism, a challenge to developing infill sites are the lengthy approval processes by municipal and provincial governments. Irwin believes these processes should be streamlined and expedited “where towers already exist.”

He’s hopeful in near future, “we’ll be able to move this idea forward.”

Irwin says he is worried about a reckoning coming with evictions as more renters have been unable to or have not paid rent.

He says data has shown about 4 per cent of renters not paying rent in Ontario every month. Pre-pandemic that number was about 1 per cent.

He adds that about 100,000 families in the province “are not able to meet their obligations.” He says FRPO members are trying to work with their residents; some are on payment plans, but as time goes on, this is “becoming more of a challenge — especially for smaller landlords.”

He says some cities such as Toronto have rent banks to help tenants, but he believes more needs to be done to solve the mounting problem.

Irwin cites the Ontario-Canada Emergency Commercial Rent Assistance Program as an example of how a program could be funded on the residential side.

“It’s an idea we’ve been talking about from the beginning,” he says. He would like to see something like an “Ontario Rental Assistance Program.”

He says FRPO, through its actions and advocacy, is continuing to have conversations with the provincial leaders to avert a wave of evictions.

The vacancy rate of the Greater Toronto Area (GTA) reached a 14-year high of 3.4 per cent in 2020, up from 1.5 per cent in 2019, says Dana Senagama, senior specialist, Market Insights for CMHC.

“The economic fallout of the pandemic has impacted the GTA rental market,” she says “causing vacancy rates to reach record highs in 2020.”

The highlights of the CMHC Toronto GTA 2020 Rental Market Survey written by Senagama are:

- Lower rental demand combined with supply growth increased primary and secondary vacancy rates in 2020.

- Despite higher vacancy rates, rents were resilient in the primary rental market

- While vacancy rates rose across the GTA, they were highest in Toronto’s downtown core.

The COVID-19 pandemic caused lower rental demand as more lower income jobs were lost and younger workers lost their jobs; the borders closed, halting immigrants and non-permanent workers from entering Canada; and university and college students stayed home taking classes virtually rather than living on or near campuses.

The three segments above make up a significant share of renter households.

The Toronto Census Metropolitan Area (CMA) recorded the highest share of rent arrears in Canada with about 11 per cent of all units reporting arrears in rent payments, according to Senagma’s report.

Adding to the higher vacancy rate in the GTA is the increase in construction of purpose-built rental units. Rental apartment starts grew by 5,720 units (measured over the 12-month period ending July 30, 2020), which is 67 per cent higher than the same period in the previous year (2,690), Senagama says. Also, rental apartment completions during the same period have remained high.

The Durham region saw the largest percentage growth of rental apartments (4.2 per cent). Given its relative affordability and improved transit systems, it remains attractive to individuals who commute or telecommute.

Much of the increase in supply continued to come to Toronto, explaining the higher vacancy rate in the city at 3.7 per cent.

Toronto, which historically boasts the highest rents and rent growth, saw the lowest rent growth in 2020, Senagama says.

Despite higher vacancy rates in the GTA, rents grew year over year from October 2019 to October 2020. But a lot of that can be attributed to strong rental growth before the COVID-19 pandemic, which skewed average rents upward.

She says many landlords used incentives such as lower deposit fees, free months of rent, free utilities/parking, and move-in cash bonuses to attract potential tenants.

Rents faced by prospective tenants remain significantly higher than those of existing tenants. In the GTA, the average asking rent for vacant units ($1,817) was 20 per cent higher than the average rent for occupied units ($1,513).

Regardless of the pandemic, affordable housing remains a challenge in Toronto and the GTA, Senagama says.

For renters whose average annual household income is below $25,000, vacancy rates are zero per cent for one- and two-bedroom units.

For those earning between $25,000 and $69,000 yearly, 69 per cent can afford to rent in the primary stock of purpose-built rentals, but Senagama says “renting in the secondary market is still relatively unaffordable for these households (the average condominium apartment rent is $2,319).”

7. MONTREAL

Sébastien Lavoie, chief economist at Laurentian Bank Securities, believes “a new normal is taking shape” from the COVID-19 pandemic, which will have a profound effect on rental markets.

He says the Canadian rental market is being reshaped by among other reasons the work-from-home phenomenon, immigration, tourism and travel, and jobs.

He says U.S. and Canadian surveys indicate a preference from employees and employers to continue the work-from-home era even if only partially.

“Both realize teleworking saves time and money,” Lavoie said.

Studies show close to half of the occupations in Toronto, Vancouver and Montreal are suitable for teleworking, compared with less than 40 per cent elsewhere in the country, he says.

So, the trend of tech and other office workers moving to smaller cities and areas around the large metro areas of Toronto, Montreal and Vancouver to find larger homes and a home office will continue.

But Lavoie believes Montreal’s rental pricing has been and will continue to be less affected overall than Toronto and Vancouver.

Toronto and Vancouver’s core areas are more subject to a decline in monthly rents because of the expensive cost per square foot, he says. “For instance, we see tighter housing conditions in Oshawa, Belleville and Hamilton. In B.C., conditions in the Fraser Valley are tighter than in the Vancouver area.

“In our view, the soft spot in the Montreal rental market is more limited than in Toronto and Vancouver,” Lavoie says.

Montreal only has a few expensive sectors, including Ville-Marie, seeing renters flee the city life for smaller cities, and paying less rent for bigger units to include the home office, he says. Thus, as renters leave the higher-priced areas, vacancies rise and rents fall.

Elsewhere on the Island of Montreal, demand for rentals remains high. Housing conditions are even more dynamic on the North Shore, he says, and even farther north to Mont Tremblant. Conditions on the South Shore are tighter than on the Island.

This divergence in rental pricing between expensive rentals in core downtowns and less dense suburbs and nearby cities and towns is likely to be a key theme of 2021, according to Lavoie.

He also cites a recent U.S. National Association of Realtors’ study, saying millennials are more flexible, looking for larger rooms, more rooms, larger units, more nearby parks.

“We think the behaviour is similar for all Canadians,” he says.

Immigration and when it will come back is one of the big questions for the rental market, Lavoie believes.

“After the worst year in immigration since the 1990s,” Lavoie says, “We find the federal government’s target to welcome 401,000 new residents in 2021 too ambitious.”

He says “Canada’s 2022 target of 411,000 new residents is a more realistic goal.”

Based on the best-case scenario, herd immunity will not be reached until the third quarter of 2021. So, Lavoie is not confident the federal government will allow 400,000 new residents into Canada this year.

Thus, he expects rental demand to strengthen in 2022 and not 2021.

“We can realistically expect higher monthly rents in 2022,” he says.

The closed border and lack of tourism are hurting Canada’s three largest cities for jobs, housing and revenue, and Lavoie believes its comeback to pre-pandemic levels will lag behind other sectors.

He says besides hurting the economy and housing, the lack of tourism is disproportionately affecting younger workers, putting them out of jobs and out of rental units. They mostly go back to live with their families, he says.

The strong pace of rental home building in Montreal before the pandemic will translate into a moderate increase in the vacancy rate. Without the pandemic, the vacancy rate would have increased modestly, he says.

The vacancy rate in the Montréal area increased to 2.7 per cent in 2020 from 1.5 per cent in 2019, according to Francis Cortellino senior specialist, Market Insights for CMHC.

“Two distinct trends were observed on the Greater Montréal rental market this year,” says Cortellino, “Vacancy rates rose sharply in large buildings in the city’s central areas, while the proportion of vacant units generally remained stable elsewhere in the metropolitan area.”

The highlights of the CMHC Montréal 2020 Rental Market Survey written by Cortellino are:

- The vacancy rate increased in 2020, reaching 2.7 per cent. However, it remained stable in the suburbs, at 1.2 per cent, while it doubled on the Island of Montréal, reaching 3.2 per cent.

- The easing of the market on the Island of Montréal was in part due to a substantial increase in vacancy rates in medium-sized and large rental towers in the city’s central areas.

- A decrease in net international migration, the absence of in-person university courses and the return to the long-term rental market of tourist-oriented rental units all contributed to vacancy rate increases.

- The average rent in Greater Montréal increased by 4.2 per cent in 2020, the largest increase since 2003.

The increase in the vacancy rate was partly due to larger rental buildings (in terms of number of units) in the following central areas: downtown Montréal, Le Sud-Ouest (likely Griffintown), Plateau-Mont-Royal and Côte-des-Neiges/Notre-Damede-Grâce.

“These areas are characterized by a high number of students, immigrants and non-permanent residents, with international students, temporary workers and asylum seekers,” Cortellino says. “These groups were significantly affected by the COVID-19 pandemic, which led to a significant decline in rental demand in these areas.”

On the supply side, about 10,600 new rental apartments were added to the Montréal CMA’s rental stock between October 2019 and October 2020, a record for the last 30 years, he says. “Eighty percent of these new units were in the suburbs, but demand was strong enough to keep the vacancy rate unchanged.”

Without tourists, Montréal experienced — along with other Canadian cities — many short-term rentals being converted to the long-term rental market, which added to supply.

Suburban rental demand was supported by among other things, a shift away from the Island of Montréal because of the pandemic, older folks selling their homes to re-enter the rental market, and the increasing propensity of younger renters to find places in the suburbs rather than Montreal and rather than being close to universities.

According to the latest survey, Montrealers made fewer moves in 2020 during the survey time. Cortellino says 11.4 per cent of renter households in the Montréal CMA had moved to a new apartment in the previous 12 months. The proportion was similar on both the Island of Montréal and in the suburbs, but lower than that recorded last year (15.7 per cent).

With all of the lockdown and sanitary measures that disrupted the lives of Montréalers at a time of the year when many decide whether to move, it appears that renters were much more reluctant to move this year, Cortellino says.

The average overall rent increase in 2020 of 4.2 per cent in the Montréal CMA has not been seen since the early 2000s, says Cortellino. But rent increases also varied greatly by major geographic area, ranging from 2.2 per cent in Laval to 4.6 per cent on the Island of Montréal.

The difference in rent between a rented two-bedroom apartment and one still on the market was 46 per cent ($895 versus $1,304, respectively) in 2020, he says. The difference varied by major CMA sector: 47 per cent on the Island of Montréal, 50 per cent in Laval, 23 per cent on the North Shore, and 29 per cent on the South Shore.

8. VANCOUVER

Vancouver’s rental market in the first half of 2021 will not be significantly different from what landlords and tenants experienced during most of last year.

“We don’t see many changes to the average monthly rental rates in the first half of 2021,” says Brock Lawson, manager, rental data for British Columbia, Urban Analytics. “We’re still facing the same challenges in today’s landscape as we were in 2020.”

Those challenges include a continuing state of emergency in British Columbia, post-secondary institutions restricting or limiting in-person classes and little to no immigration. In short, the pandemic continues to dominate market trends.

Lawson foresees several of the trends driven by the COVID-19 pandemic continuing.

He believes renters will continue to seek housing opportunities in suburban locations where they’re finding more value in terms of living space. This trend is driven primarily by the increase in the number of people working from home. Living and working in the same space has obviously proven challenging for many, and if the majority of employees continue to work remotely, demand should remain strong for suburban rentals that offer larger living spaces.

In terms of trends with staying power, Lawson believes landlords and tenants alike will continue to make use of virtual and online showings. “We saw this trend emerge before the pandemic, but it grew increasingly popular throughout the year,” he says.

The same can be said for automated leasing procedures that can be executed virtually, which will also likely continue post-pandemic.

As for the use of incentives, Lawson doesn’t anticipate landlords will drop them any time soon. “I foresee these continuing into 2021,”he says. “Incentive programs have been successful, and demand hasn’t yet returned to pre-pandemic levels.”

Lawson believes the primary reason the market continues to see high-value incentives is rent control measures. The freeze on rents until July of this year, combined with the policy of limiting rent increases to the rate of inflation, has led developers and landlords to seek the highest possible contract rents to establish an elevated benchmark to which future increases can be applied. This, according to Lawson, is why Vancouver landlords and property owners continue to offer top-flight incentives rather than lower overall rents: The incentives allow prospective tenants to pay lower effective rents while enabling owners to maintain higher contract rents.

The increasingly popular method of metering utility costs per tenant, as opposed to including them in rent, will also continue in 2021 — thus transferring more of the operating costs from owners to tenants.

But Lawson points to a slow and expensive approval process, development fees and rent control policies, as impediments to the long-term viability of rental development in Vancouver.

Approximately 3.6 million square feet of office space is under construction, with an additional two million square feet under review in Downtown Vancouver alone. Of that space, 64 per cent is already pre-leased. Yet, between 2018 and 2020, less than 4,000 purpose-built rental units were completed each year across the entire Metro Vancouver region.

“The new level of rental supply will not come close to meeting the demand for product,” says Lawson, “especially once immigration resumes and post-secondary institutions return to in-person classes.”

As the manager of Urban Analytics’ rental data platform, Lawson anticipates Vancouver will begin to see that rise in rental demand and a modest increase in rental rates in the second half of 2021.

“Vancouver needs to continue its growth in supply,” Lawson says, “to meet and keep up with demand levels that will be seen as we start to work our way back from the COVID-19 pandemic.”

The overall vacancy rate for purpose-built apartments in the Vancouver Census Metropolitan Area (CMA) increased to 2.6 per cent in October 2020 from 1.1 per cent the year before, says Eric Bond, senior specialist, Market Insights for CMHC.

This is the highest vacancy rate in the Vancouver CMA since 1999, and comes after six consecutive years with vacancy rates close to 1 per cent, he says.

“Higher supply and lower demand combined to increase the vacancy rate in Vancouver CMA,” Bond says, “But there are important differences between market segments and geographies.”

The highlights of the CMHC Vancouver 2020 Rental Market Survey written by Bond are:

- The purpose-built rental apartment vacancy rate increased from 1.1 per cent in 2019 to 2.6 per cent in 2020 due to higher supply and lower demand. Newer structures in central areas drove the increase in the vacancy rate, while vacancy rates decreased in suburban markets.

- The pace of average apartment rent increase slowed to 2 per cent; however, prospective tenants face higher rents than longer-term tenants, with the average asking rent for vacant units being 21.4 per cent higher than the average rent paid for occupied units.

- While the overall rental market loosened somewhat in 2020, new rental affordability data show that significant imbalances remain, posing challenges for lower income renter households.

- The number of condominium apartments in long-term rental increased by 10.2 per cent (7,137 units) as investor-owners increased their involvement in the long-term condominium rental market.

Newer structures and those in central areas saw larger increases in vacancy rates, particularly for high-rise structures with 200 or more units.

Vacancy rates decreased in suburban markets with lower rents, a trend that also extended to tighter rental market conditions in nearby cities such as Abbotsford-Mission, Bond says.

These regional differences in the vacancy rate are consistent with the findings in other large Canadian centres, such as Toronto and Montreal, where demand has shifted away from downtown cores to more outlying areas and neighbouring cities.

Rental demand was lower in Vancouver – as in other major metropolitan areas – because of employment losses especially for younger workers in the service industries; slower migration with the borders closed and university and college students taking classes online and not returning to campuses.

“In the University Endowment Lands, home to the University of British Columbia, the purpose-built rental apartment vacancy rate increased from 0.4 per cent in 2019 to 13 per cent in 2020,” Bond says. “The supply of units in this area did not increase during this period, suggesting that this change results purely from a reduction in demand.

Bonds says entry-level home prices continue to remain high relative to local incomes, resulting in many potential home buyers facing financial barriers to entry into home ownership. Some potential homebuyers might be choosing to rent longer term, contributing to high baseline rental demand.

Same-sample average rents for apartment units in the Vancouver CMA primary rental market increased 2 per cent overall, down from 4.7 per cent in 2019, he says. Some high rent central areas of Vancouver saw rents move lower, namely in English Bay (-2.4 per cent) and Kitsilano/Point Grey (-1.3 per cent).

“The average asking rent for vacant units was 21.4 per cent higher than the overall average rent for occupied units in the Vancouver CMA,” Bonds says. This gap suggests that market rents faced by prospective tenants continue to see upward pressure following several years of strong demand that raised rents significantly, while tenants remaining in the same unit only face rent increases in line with the provincially allowable amount.

In the Vancouver CMA, average rents for new two-bedroom units ($2,554) exceeded both the asking rent ($2,157) and occupied rent ($1,781) for two-bedroom units of all ages, revealing the significant premium for newer units, he says. Overall vacancy rates were also much higher in new structures (9.1 per cent) compared with the structures of all ages (2.6 per cent).

On the condominium side, with new units coming on the market and some owners converting short-term rentals to long-term residences, the proportion of condominiums being rented long-term increased to 29.6 per cent in 2020 from 28 per cent in 2019.

For affordable housing, only 0.2 per cent of the Vancouver CMA rental stock would be affordable to renter households with $25,000 or less annual income, he says, while households making $47,000 or less annual income can access only 23.9 per cent of the rental market. Of these units, only 12 per cent have two or more bedrooms, highlighting the challenges for families with incomes in these ranges.

“While the overall rental market loosened somewhat in 2020, Bonds adds, “these results reinforce that significant imbalances and pressures remain, particularly for lower income renter households.”

9. CALGARY

The overall apartment vacancy rate in the Calgary CMA rose to 6.6 per cent in October 2020 from 3.9 per cent a year earlier, says Michael Mak, senior analyst, economics for CMHC.

“Pandemic related impacts, oil sector job losses, and continued rental supply increases led to increased vacancy rates,” Mak says.

Calgary saw a steady pace of rental building completions in 2020 at an increase of 3.2 per cent compared to 2.8 per cent in 2019.

The Downtown had the largest vacancy rate increase at 8.8 per cent this year vs. 3.4 per cent in 2019, Mak says.

The highlights of the CMHC Calgary 2020 Rental Market Survey written by Mak re:

- The apartment vacancy rate in the Calgary CMA rose to 6.6 per cent, a level last seen in 2016.

- The average rent in Calgary rose slightly to $1,195, as property owners use non-price measures to compete for tenants.

- Rental supply in both primary and secondary rental markets grew by 2.5 per cent (1,650 units), led by a higher increase in primary rental units.

The effects of COVID-19 have hurt the economy and decreased rental demand. Unemployment has risen because of the pandemic and the oil market problems.

Mak says while the unemployment rate in October 2020 was 11.5 per cent — lower than the peak of 15.3 per cent in July — unemployment in Calgary remains high compared to the 7.6 per cent unemployment rate in October 2019. Employment in the 15-24 age group was down by 14.6 per cent in the same period.

The border closure and restricted immigration also added to decreasing rental demand in Calgary.

Average rents were flat in Calgary for all bedroom types, despite rising vacancy rates and lower employment, providing evidence that property managers are using incentives such as free utilities, lower deposit fees, cash bonuses, and free rent to drive demand for rental units, Mak says.

The average two-bedroom rent was $1,323 in Calgary, with the Beltline zone continuing to command the highest rent at an average of $1,447 for a two-bedroom.

Vacant and occupied units in the CMA had a slight difference, with average rents in vacant units 4.4 per cent higher than rents in occupied units. This is in contrast to other major centres such as Vancouver and Toronto, where the average difference is over 20 per cent.

Forty-five percent of the rental supply increase in 2020 was in the Downtown and northwest, where 26.7 per cent of Calgary’s primary rental apartments are. The southeast also had an 11.5 per cent increase in rental supply this year, while containing 6.2 per cent of Calgary’s primary rental supply.

An affordability gap remains for Calgary’s lowest wage earners, Mak says. Households with income below $36,000 a year have access to 11 per cent of the rental universe in the CMA.

“This means that the lowest income earners consisting of 20 per cent of Calgary’s rental household population, can reasonably afford 11 per cent of existing units,” Mak says.

Many households would have to pay above the 30 per cent threshold, since earners above this income level could also choose to rent in the lower rent segment, competing against the low wage earners

Andie Daggett, vice president, sales and client experience at Urban Analytics, doesn’t expect to see much change in the rental market of either Calgary or Edmonton until at least the third quarter of this year.

Daggett was recently promoted to her new role from manager of rental market data at Urban Analytics.

“The first half of 2021 will continue to see stable rents, as owners and developers continue to navigate the current economic conditions facing renters,” she predicts.

That said, Daggett believes the COVID-19 vaccine rollout will have a positive effect on the economy, allowing for more availability and job stability, leading to an influx of qualified prospects looking to rent. Consequently, owners and developers are likely to begin increasing rents in the second half of 2021.

Calgary and Edmonton’s rental markets were competitive in 2020, due in part to the offering of incentives to both retain tenants and attract new prospects. Many projects were in the market with one-month-free incentives or discounted monthly rents. Some were offering up to three months free, she says.

The proliferation of incentives was a direct result of new product launches in a pandemic-impacted market. This created a domino effect and resulted in older buildings, plus buildings in suburban areas of both cities, competing with downtown projects.

Daggett foresees incentives continuing into this year. “It would be very difficult to remove a rental rate incentive,” she says, “without risking tenants moving out because they could no longer afford their rent.”

What else is likely to prevail post-pandemic? Virtual tours.

“They are very convenient for both the tenant and leasing agent,” says Daggett. “They take less time and are easier to organize for both parties: Leasing agents can show more units, and renters can view more buildings, speeding up the application and lease-signing process.

“They are a win-win for both parties.”

Another pandemic-influenced trend Daggett foresees is higher demand for larger living spaces. With many people likely to be working from home for much of this year, they’re seeking residences that can accommodate both working and living spaces. She believes Calgary and Edmonton projects will offer a greater proportion of larger floor plans.

“If you’re not required to go into your office downtown, you could live in a more affordable area of the city without having to worry about commuting,” she says.

One of the biggest difference-makers in the coming year is the potential reinstatement of in-person classes at post-secondary institutions. The return of post-secondary students to campuses, if it happens this year, will impact vacancies and rents in both cities. Says Daggett: “Rental property owners and developers should be prepared for either scenario and adjust their offerings and marketing programs accordingly.”

As is the case in many urban centres across the country, the urban cores of Calgary and Edmonton have become increasingly competitive, and are likely to remain so for the foreseeable future given the amount of product planned for these areas. “Developers should consider opportunities in areas that are underserved,” says Daggett, “such as more established inner-city suburban communities.”

In terms of economic forecasting, Daggett says, “There is an uncertain economic outlook in both Calgary and Edmonton, especially for higher end products. Government incentives could create more opportunity for new companies to establish operations in these cities. Both cities require more diversification in their economies to prevent uncertainty.”

10. EDMONTON

The purpose-built rental apartment vacancy rate in the Edmonton CMA increased to 7.2 per cent in October 2020 from 4.9 per cent in October 201, the highest since 1997, says Christian Arkilley, senior analyst, economist, CMHC.

“Slower rental demand due to weaker economic conditions and lower migration combined with higher rental supply resulting in an increase in vacancy rate in the Edmonton CMA.” Arkilley says.

Despite the increase in apartment vacancy rate, the overall average rent was statistically unchanged at $1,153 in October 2020, compared to $1,144 in October 2019.

The highlights of the CMHC Edmonton 2020 Rental Market Survey written by Arkilley are:

- The purpose-built rental apartment vacancy rate increased to 7.2 per cent due to lower demand and higher supply.

- Despite the increase in overall vacancy rate, there was no significant change in average rents.

- Market conditions continue to be tight in the condominium apartment segment, resulting in a decline in the vacancy rate.

The average rent for new units in structures completed in the past two years was $1,513, that’s 31.2 per cent higher than the average rent of purpose-built rental units of all ages. The vacancy rate for these newer units was also higher at 12 per cent, Arkilley says.

While rental completions in the Edmonton CMA more than doubled over the past year with 2,223, demand for rental units weakened over the past year, with the economy being affected by both the COVID-19 pandemic and the fall in oil prices.

Arkilley says the region experienced consistent job losses since the beginning of 2020 (over 121,000 job losses in the first half of 2020) predominantly among the younger demographics (20 per cent for ages 15-24 and 65 per cent for ages 25-44) who are primarily renters.

Travel restrictions due to the COVID-19 pandemic have limited international migration, which contributed to 50 per cent of the population growth in 2019. In Q2 2020, Alberta’s international migration declined by 93 per cent compared to Q2 2019, while non-permanent residents left the province, he says. The decrease in migration had a negative impact on rental demand since new migrants tend to form renter households.

On the affordability front, renter households with annual income of less than $36,000 can only afford the first 15.1 per cent of the rental stock within the Edmonton CMA, he says. About a quarter of the households with annual income of less than $36,000 are spending more than 30 per cent of their income on rent.

“Despite greater rental affordability than many other Canadian cities,” Arkilley says, “challenges remain in the Edmonton CMA, especially for low-income households seeking larger units.”

11. OTTAWA

Rich Danby, founder of Rich Ottawa Investments and OttawaHousePainters.com, believes predicting what will happen in the rental market in 2021 with COVID-19 resurging is “anybody’s guess.”

But the real estate investor, coach and speaker is confident in the stability of the Ottawa rental market.

“Ottawa is typically not as prone to market swings as other cities in Canada when it comes to unknowns such as stock market crashes or even pandemics,” he says.

The rental market in Ottawa has grown in the last couple of years, and demand is still high, Danby says.

Average monthly asking rent in December for a one-bedroom home on Rentals.ca was $1,565 and $1,993 for a two-bedroom.

Even with the shutdown, the market is doing well, he says, “Ottawa is a stable place to buy, if you buy what people need – one-, two- and three-bedroom properties.” He says demand for three-bedroom homes is and will be stronger as people continue to work from home and look to add space for a home office.

People will always need to rent, he says, if businesses shut down and people have to sell their homes, they will have to get back into a rental for a place to live.

Danby believes 2021 needs to be the year of the landlord.

His message to those managing properties: “Show you tenants how much you love them.”

His advice for landlords is to communicate directly with tenants, find ways to work with them, be a more hands-on property manager – even offering incentives for paying rent on time.

He says management will be the key in 2021 to staying out of messy evictions, which are not only increasing, but are also obviously challenging.

“You hate to lose one or two months rent,” he says, but it would be better than going through the eviction process. Of course, when tenants don’t pay for an extended time, tough decisions have to be made, he says.

But Danby believes 2021 could come down to being like other years for the rental market – dependent on supply and demand.

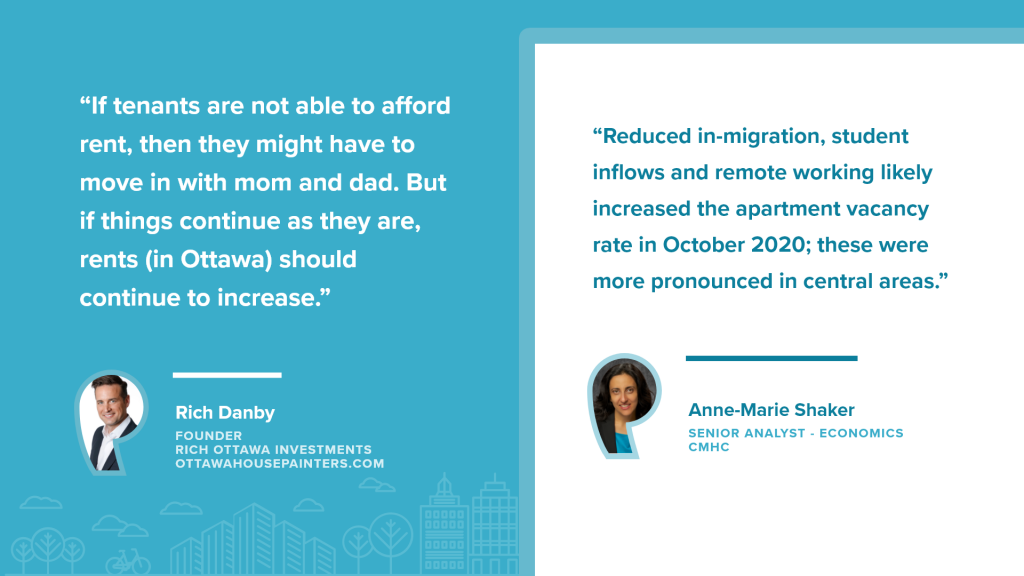

“If tenants are not able to afford rent, then they might have to move in with mom and dad,” he says. “But if things continue as they are, rents (in Ottawa) should continue to increase.”

The purpose-built apartment vacancy rate in Ottawa was 3.9 per cent, up from 1.8 per cent a year earlier, according to the Rental Market Survey conducted in October 2020.

With few exceptions, the vacancy rate rose in more centrally located areas, affected by reduced student and young professionals’ demand, while outer suburban areas — less affected by such demand — either declined (East Ottawa) or the change was not significant (West Ottawa, says Anne-Marie Shaker, senior analyst, economics for CMHC. Shaker wrote the Ottawa report.

“Reduced in-migration, student inflows and remote working likely increased the apartment vacancy rate in October 2020,” she says, “These were more pronounced in central areas.”

The highlights of the CMHC Ottawa 2020 Rental Market Survey written by Shaker are:

- The overall vacancy rate for purpose-built rental apartments rose from 1.8 per cent to 3.9 per cent on weaker demand and rising supply relative to October 2019.

- The average fixed-sample rent for two-bedroom apartments increased at a robust 5.2 per cent but lower than last year’s 8 per cent.

- Arrears in the Ottawa CMA were among the lowest in the country supported by the relative stability of the labour market.

Sandy Hill/Lowertown, where Ottawa University is, together with Alta Vista had the highest vacancy rate at 6.7 per cent each, Shaker says.

The decline in student demand likely pushed vacancies higher in Sandy Hill/Lowertown, while the rise in vacancy in Alta Vista was likely partly due to the area’s considerable share (12.2 per cent ) of newly constructed units, she says. The area also had the second highest average asking rents in the Ottawa CMA.

New units tend to have a higher vacancy as they are being absorbed in the market, as well as higher rents than existing market averages, Shaker says. Chinatown/Hintonburg/Westboro also registered an increase in vacancy rate, recording the fourth highest overall vacancy (4.6 per cent) in the CMA.

“Although the vacancy rate rose, Ottawa’s rental market and its housing market in general have been supported by the relative stability in public administration employment,” Shaker says.

Rent payment arrears in Ottawa are among the lowest for Canadian CMAs at 3.5 per cent.

The fixed sample average rent for the benchmark two-bedroom apartments increased 5.2 per cent, surpassing the Ontario rent increase guideline of 2.2 per cent for 2020, but was lower than last year’s 8 per cent.

12. WINNIPEG

There is no easy answer to the question: Will rents in Winnipeg go up this year?

With rent controls in place, Avrom Charach, vice-president of Kay Four Properties Inc., believes there are two ways to look at the issue of average rents. He sees registered rents climbing by more than Manitoba’s CPI-based 1.6 per cent guideline for 2021.

“I believe the average increase will be in the range of 4 per cent, because operating costs increase by more than inflation,” he says, “And new units are coming online for which rents are always higher than average market rent.”

Yet Charach maintains it’s important to consider what tenants are willing to pay, which he believes will be an increase of no more than 2 per cent. “This is in part because we have new stock coming online,” he says. “That, coupled with low interest rates, will see tenants with employment looking to purchase homes, while tenants still suffering from COVID-related stress will be unable to absorb increases.”

That said, Charach predicts “Manitoba’s market, especially in Winnipeg, will remain a tenant’s market with a vacancy rate exceeding 3 per cent.”

The impact of the pandemic on Winnipeg’s rental market is arguably less than in other urban centres in the country, as average rents in Winnipeg are lower than the Canada Emergency Response Benefit (CERB). However, the pandemic’s impact on the economy has led some renters to take on more roommates, while others have struggled to keep up with rent now that CERB has ended.

As a result, Charach believes the city’s landlords will see more challenges with rents being paid on time, at least until the fall of this year, “and perhaps even through the first few months of 2022 — at least until some new normal is achieved.”

With the continued development of new housing stock (including many condominiums), Charach anticipates competition for tenants will heat up, leading the city’s landlords to become more aggressive with renovations and upgrades. Plus, “landlords will look to hold on to good tenants through discounts and other means,” he says.

Charach points to Winnipeg’s highly regulated market as one of the city’s biggest challenges in 2021. Unlike other Canadian jurisdictions, Winnipeg doesn’t have mark-to-market rent among tenants.

“Also, with COVID-19 creating the financial issues it has for tenants and government,” he says, “We see the potential for increased scrutiny and attempts to find ways to get more fees or taxes from our industry.”

The Winnipeg CMA apartment vacancy rate rose to 3.8 per cent in October 2020, the first increase since 2015, says Heather Bowyer, senior analyst, economics for CMHC.

“The vacancy rate increased in the Winnipeg CMA for the first time since 2015,” Bowyer says, “as continued additions to new rental supply outpaced weakened demand.”

While 2020 rental construction continued its strong pace as seen in previous years, rental demand was hampered by the COVID-19 pandemic.

The highlights of the CMHC Winnipeg 2020 Rental Market Survey written by Bowyer are:

- The apartment vacancy rate rose in the Winnipeg CMA to 3.8 per cent as supply increased and demand for rental units slowed.

- The average apartment rent increased 3 per cent over the past year as weaker rental demand limited rent growth compared to previous years.

- While rental demand remains high for affordable units, new rental supply tends to have higher average rents.

Lower rental demand can be attributed to the higher unemployment rate – up to 9 per cent and reaching 17 per cent for those ages 15 to 24; a big decline in immigration, international students and other non-permanent residents with the border closure; and online classes replacing students in campus classrooms and in rental units.

Between the third quarter of 2019 and the second quarter of 2020, 1,152 rental apartment units were added, primarily in the East Kildonan, Fort Garry, and Centennial survey zones, she says.

And, as of October 2020, Bowyer says, 2,744 apartment units were under construction in the Winnipeg CMA, which will increase supply as these units reach completion in the coming years.

“The average asking rents for vacant apartment units was $75 more or 7 per cent higher than those paid for occupied units, which represents a widening of the gap compared to 2019,” says Bowyer, “Given this larger differential, tenants may be less inclined to move to a new unit, as reflected in the lower apartment turnover rate in 2020 of 13.6 per cent compared to 24.4 per cent in 2019.”

But, she adds, this lower turnover rate is also likely reflective of tenants’ reluctance to move during the COVID-19 pandemic.

Weakened rental demand limited the growth for average overall rents to 3 per cent in October 2020, a decrease from 3.5 per cent in 2019, she says. Accounting for both new and existing structures, the average rent was $1,107 in October 2020. Rents ranged from a low of $849 in Lord Selkirk, which has older rental stock, to $1,565 in outlying areas of the CMA where newer, larger units are.

For affordable housing, those with incomes of less than $25,000, experience the lowest vacancy rates in the Winnipeg CMA at 2.9 per cent, suggesting there is higher demand for more affordable units. Only 3 per cent of the total rental stock is affordable in this lowest income segment Bowyer says.

Also, much of the new rental stock coming onto the market has higher rents, which poses a challenge for the already small number of units available to low-income households, she says. In the past two years, 2,465 rental units were added with an average rent of $1,576. This rent would be affordable to individuals with a before tax income of $63,000, which represents roughly 28 per cent of rental households.

13. HALIFAX

Average rents in Halifax are on the rise. This despite a recent rent cap of 2 per cent a year imposed by the Nova Scotia government late last year, retroactive to September.

Although this cap should control rent escalation for existing units on an individual basis for the time being, according to Neil Lovitt, vice-president of planning and economic intelligence at Turner Drake and Partners, it will likely lead to a greater number of smaller increases as property owners hedge against their now-limited ability to impose higher rent hikes.

“While we are bringing more stock to market, our rate of completions is trending a little below last year,” says Lovitt, “and that doesn’t bode well for the supply deficit that’s developed over the past four years or so. We therefore expect the continuing supply crunch to keep pressure on market rents.”

Prior to the pandemic, Halifax was experiencing a prolonged period of rental demand growth. Since early 2020, however, that demand has abated. As with elsewhere in the country, this drop has been due to a lack of immigration and the shutdown of in-person classes at post-secondary institutions.

This lessening of demand might give the market some breathing room in the first two quarters of 2021, but Lovitt expects the market to pick up as the impact of COVID-19 wanes in the latter half of the year. “We don’t expect the pandemic to permanently change the course of trends we were experiencing beforehand,” he says. “It may take another year to play out, but a return to the pre-COVID paradigm is likely.”

Unlike in other major centres across the country, COVID-19 protocols and the proliferation of residents working from home have not hollowed out central urban rental markets on the East Coast, he says.

This is just one reason why Halifax is suffering from what Lovitt calls a “dire” lack of non-market housing, and government housing in particular. Rental affordability challenges had been mounting for several years prior to the pandemic.

In Lovitt’s view, the supply shortage has impacted the lower end of the rental market where older stock is being redeveloped or recapitalized in response to strong demand and lagging construction of new supply.

“In a nutshell,” he says, “the bottom of the market is moving beyond what lower income households can absorb.”

Halifax’s owner-occupied market has been hotter than in previous years, and Lovitt expects that trend to have a trickle-down effect on the rental market.

Until recently, the market for new owner-occupied housing was sluggish. But lower interest rates and the Canada Emergency Response Benefit (CERB), coupled with an influx of new residents from other parts of the country (due, in part, to the region’s comparatively better COVID response), have fired up demand for housing.

Mortgage rates have declined as a result of the pandemic, and the Bank of Canada has come out strongly saying that they are likely to remain this low for a couple of years at least. This has increased purchasing power and given greater confidence to buyers about the longevity of that purchasing power. It all adds fuel to the fire that is the homeownership market.

“Real estate agents in the province have been very, very busy,” says Lovitt. “And this pressure will likely keep people in the rental market longer than we would otherwise have expected.”

The vacancy rate in the Halifax CMA increased by just 0.9 percentage points to 1.9 per cent in 2020, according to Kelvin Ndoro, senior analyst, economics for CMHC.

“The rental market, though easing, is still tight and in need of increased supply,” he says. Record low inventory of homes for sale likely slowed the transition from rental to homeownership, which together with increased interprovincial migration partly offset the negative impacts on rental demand.

The highest vacancy rate was in Peninsula South (3.7 per cent), an area with a high concentration of students, Ndoro says. This highlights the impact of the major universities offering their programs online.

Dartmouth City’s vacancy rate of 1.3 per cent was virtually unchanged and lower than Halifax City (2.2 per cent). Rental demand remained strong in Sackville and virtually unchanged from 2019.

He says vacancy rates also increased significantly for structures with 100-plus units, most of which are on the Peninsula. Ditching the daily commute because of work-from-home arrangements and higher average rents on the Peninsula are all possible contributory factors.

The highlights of the CMHC Halifax 2020 Rental Market Survey written by Ndoro are:

- A drop in international immigration and changes to university program delivery contributed to an increase in the vacancy rate.

- The average rent increased by 4.1 per cent despite the easing of pressure on the rental market.

- Peninsula South structures built in the last two years had a vacancy rate of 2.7 per cent and an average rent of $1,954.

Rental units added to the market in 2020 increased 2.9 per cent, Ndoro said.

COVID-19 measures significantly affected key rental market drivers. Year-to-date, international immigration was down 55 per cent between January and June of 2020.

“Full-time student enrolment was down in four of the six Halifax universities with more students enrolling part-time instead,” Ndoro says, “More than half of Halifax students do not permanently live in Nova Scotia and thus would have opted to stay away from the city with classes offered online.”

But net interprovincial migration has remained strong, he adds, increasing 8 per cent in the second quarter of 2020 compared to the same period in 2019.

The overall average rent in Halifax was $1,170, an increase of 4.1 per cent, he says. Average rents increased despite higher vacancy rates and lower turnover rates. There likely was reduced mobility due to Covid-19, and an increased likelihood for tenants to accept rent increases, aided by income support from the government.

14. HAMILTON

The overall vacancy rate in Hamilton CMA’s primary rental market was 3.5 per cent in 2020, down slightly from 3.9 per cent in 2019, according to Anthony Passarelli, senior analyst, economics for CMHC.

“Both rental demand and supply were steady, says Passarelli. “This year’s vacancy rate was similar to Hamilton’s 10-year historical average.”

The highlights of the CMHC Hamilton 2020 Rental Market Survey written by Passarelli are:

- The overall vacancy rate was unchanged as rental demand and supply were both similar to last year.

- A greater number of tenants remained in their units this year, offsetting weaker inflows of new renters.

- Factors that kept more tenants in their units included higher homeownership costs and government measures that addressed either the spread of COVID-19 or the economic fallout it produced.

- Lower international migration, fewer student renters and weaker employment conditions contributed to weaker inflows of new renters.

- Rent growth far exceeded the Ontario Rent Increase Guideline of 2.2 per cent.

Fewer renters transitioned into homeownership this year, Passarelli says, as vacancy and turnover rates for units with higher rents, such as two-or-more bedroom units and townhomes, were either steady or lower.

Also, fewer renters became homeowners because they could not afford to buy a median-priced resale home in Hamilton. Required income to qualify for a mortgage was higher in 2020, and the price of a median-priced home in Hamilton increased far more than the purchasing power of renters, he says.

Rental demand was lower in Hamilton as in other cities because of the halt to immigration and less student housing demand because of closed campuses as students took their courses online.

“Immigration, Refugees and Citizenship Canada revealed that 40 per cent fewer new permanent residents moved to Hamilton CMA in the first three quarters of 2020 compared to the same period last year,” Passarelli says. “This significantly restrained growth in the number of occupied rental units, since the vast majority of international migrants have historically lived in rental housing in their first five years in Hamilton.”

The percentage decrease in international students living in Hamilton was likely similar to Canada, which had 37 per cent fewer study permit holders living in the nation in the first three quarters of 2020 compared to the same period last year.

He says McMaster University student residences were closed this fall and nearly all classes for the fall and winter semesters were only available online due to health and safety protocols related to the COVID-19 pandemic.

Employment conditions, particularly for younger adults who are mostly renters, were much weaker in 2020.

Unemployment rates for those ages 15-24 more than doubled between October 2019 and October 2020, increasing beyond 20 per cent, Passarelli says. “The extremely high unemployment rate severely limited the number of young adults that could separate from their parents to form their own household.”

The unemployment rate for people ages 25-44 also increased significantly this year, coupled with high job uncertainty “likely prevented more renters from this age group from transitioning into homeownership,” he says.

Passarelli says the average overall rent increase for units surveyed in both 2019 and 2020 was 5.4 per cent, far more than the Ontario Rent Increase Guideline of 2.2 per cent.

Units listed for rent were on average 13 per cent more expensive than rents for occupied units, he adds.

Condominium rental apartments increased by nearly 4 per cent in Hamilton in 2020 with most of the added rental units coming from the high number of new condominium apartment completions since last year’s survey.

Rental demand for these units matched supply, keeping the vacancy rate for condominium rental apartments unchanged at a low 0.3 per cent, Passarelli says.

The supply of units renting for less than $1,000 got smaller this year as strong rent growth pushed some apartments into higher rent categories. But demand for these less expensive units likely increased due to a lack of income growth he says.

15. LONDON

The purpose-built rental apartment vacancy rate in the London CMA was 3.4 per cent in October 2020, increasing from the 1.8 per cent vacancy rate in October 2019, according to Andrew Scott, senior analyst, economics at CMHC.

“The vacancy rate increased as new supply outpaced demand due to weaker population and economic growth,” Scott says.

The highlights of the CMHC London 2020 Rental Market Survey written by Scott are:

- The purpose-built rental apartment vacancy rate increased to 3.4 per cent.

- New supply was met with muted rental demand.

- The average fixed sample rent increase for two-bedroom apartments was 6.8 per cent.

As with many other Canadian cities, London had a larger increase in supply in 2020, but had lower demand.

The municipality was not only affected by economic disruption, but also by the lack of new immigrants moving to the city with the border closed. Both were caused by the COVID-19 pandemic, and both were a driving force behind the lower renter demand.

The same was also true for temporary international migrants such as students and international students, Scott says. Demand in Northwest London and Downtown North was particularly affected by lower attendance at the University of Western Ontario. Downtown North had the highest vacancy rate in the London CMA at 5.9 per cent. Many domestic and international students likely chose to study remotely this year.

Even with the higher vacancies in 2020, Scott says the fixed-sample percentage increase in the average rent was 7 per cent for two-bedroom units in structures common to both the 2019 and 2020 surveys, up from 5 per cent a year ago. Rents increased across all bedroom types, with bachelor units seeing the largest increase at 8.5 per cent.

The increase in rents in part reflects the greater competition for units before the pandemic, he says, when vacancy rates were near record lows.

As of October 2020, Scott says average asking rent on two-bedroom vacant units were 23.1 per cent above occupied units in Southwest London, followed by Northwest London (17.3 per cent) and East London (16.8 per cent).

The vacancy rate for condominium units offered for rent was 0.3 per cent in 2020, a decline from 1.3 per cent in 2019. Scott says the market for rented condominiums bucked the trend of purpose-built rentals, as the number of units offered for rent could not keep pace with growth in demand in 2020, resulting in lower vacancies.

The average rent on a two-bedroom condominium was $1,619 compared to $1,207 for a two-bedroom purpose-built rental apartment.

Scott estimates that only 2.3 per cent of the rentals in the Rental Market Survey were affordable to households in the lowest income level. This group can afford a monthly rent of less than $625. The rental universe becomes more affordable for those in the next income level, where an estimated 24 per cent of rentals would be within reach. But the vacancy rate for units in this rent range was well below average at 1.6 per cent.

16. VICTORIA

The vacancy rate of the purpose-built rental apartments in the Victoria CMA increased to 2.2 per cent in 2020 from 1 per cent in 2019, the first time it has surpassed 2 per cent since 2013, says Pershing Sun, senior analyst, economics for the CMHC.

“Rent growth remains robust despite higher vacancies, highlighting rental affordability challenges amid pandemic uncertainties,” Sun says.

The highlights of the CMHC Victoria 2020 Rental Market Survey written by Sun are: