The average rent for all Canadian properties listed on Rentals.ca in September was $1,769 per month, down 9.5% annually. The average rent has been nearly identical over the last four months between $1,769 and $1,771.

1. National Overview

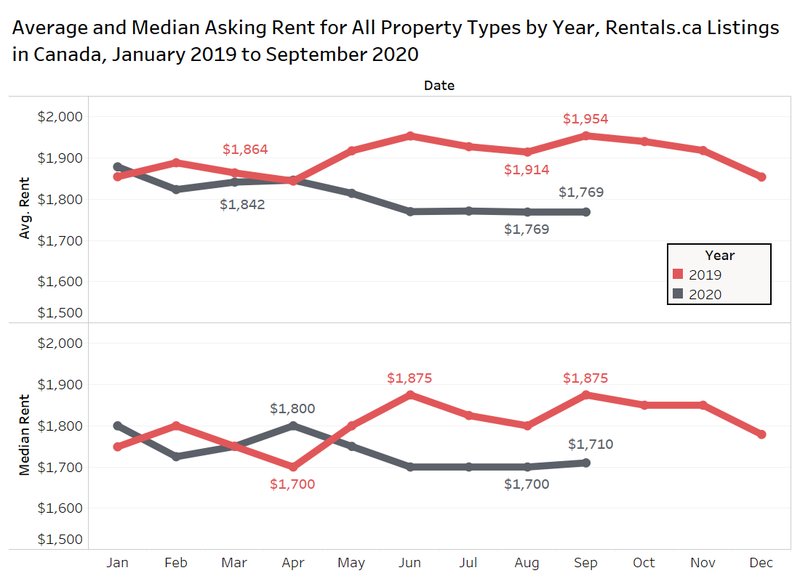

The chart below shows the average monthly asking rent for single-family housing, townhouses, rental apartments, condominium apartments, and basement apartments cumulatively from January to September of this year (black) and last year (red). The top panel shows the average rent, with the bottom panel showing the median rent.

Prior to the pandemic, rental rates in both years were following a similar path, but 2020 dropped off during the early months of the pandemic and has stayed flat since.

Quarterly Rents by bedroom Type

Quarterly Rents by bedroom Type

September marked the end of the third quarter, and looking at trends on a quarterly basis can eliminate some of the volatility with smaller monthly sample sizes.

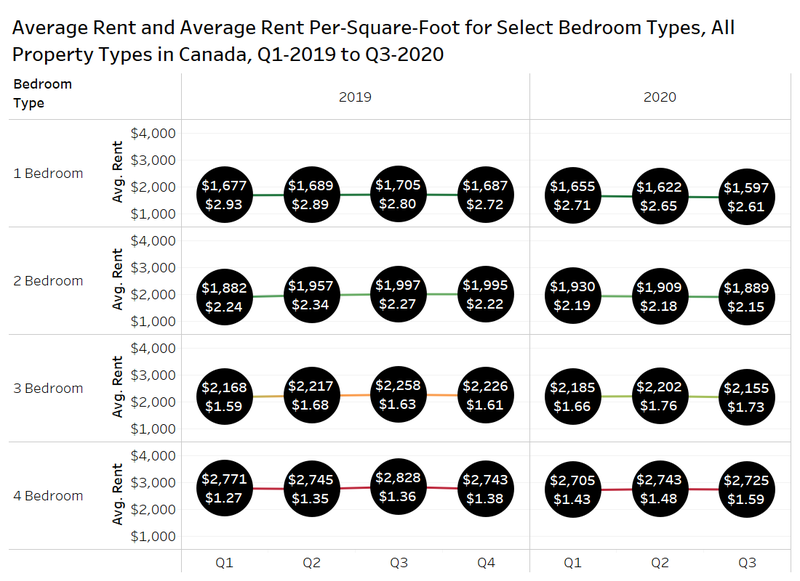

The next chart looks at the average rent and average rent per square foot for all property types by the number of bedrooms (one-bedroom to four-bedroom units only).

The average monthly rent is down for all bedroom types shown above, with one-bedroom suites falling 6.3% annually to just under $1,600. Two-bedroom units fell by 5.4% year over year to about $1,890 per month.

The average monthly rent is down for all bedroom types shown above, with one-bedroom suites falling 6.3% annually to just under $1,600. Two-bedroom units fell by 5.4% year over year to about $1,890 per month.

Three-bedroom units in the third quarter declined from $2,258 per month to $2,155 per month, a 4.6% decline. Four-bedroom homes saw the smallest drop (-3.6%) to $2,725 per month, as many tenants working from home seek out larger units to accommodate one, two or even more people working from home.

Change in Rent by Rounded Unit Size and Property Type

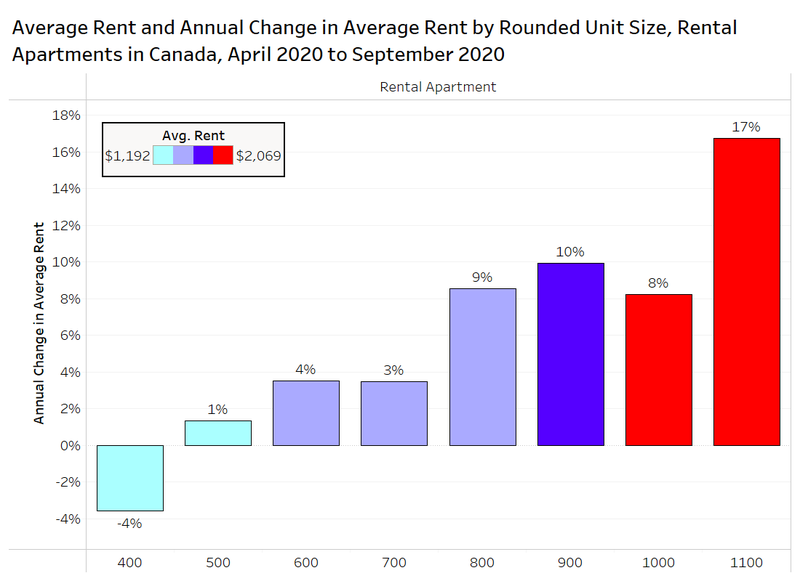

With many tenants seeking more space due to working from home, it is worth looking at whether that is impacting rental rates by unit size. To better isolate the impact of a unit’s square footage, concentrating on one property type is ideal. The chart below looks at the annual change in average rent for apartments by rounded unit size (rounded to the nearest hundred) for the pandemic period of April to September 2020 versus the same six months last year (units from 350 square feet (sf) to 1,149 sf only).

The data confirms our theory conclusively. Rental apartments around 400 sf have seen average rents decline by 4% annually in Canada, while 1,100-square-foot rental apartments have seen average rents increase by 17%, with a visible stepping up for the unit sizes in between.

When looking at the change in listings on Rentals.ca by rounded unit size (not shown in the chart), the “stepping” is completely reversed, with the biggest growth in listings occurring for 400-square-foot listings, and the smallest growth in listings for 1,100-square-foot units.

When looking at the change in listings on Rentals.ca by rounded unit size (not shown in the chart), the “stepping” is completely reversed, with the biggest growth in listings occurring for 400-square-foot listings, and the smallest growth in listings for 1,100-square-foot units.

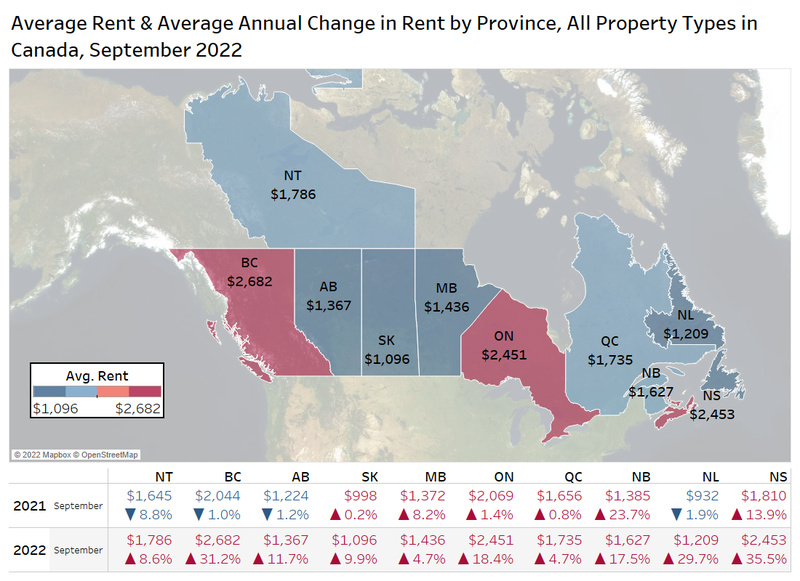

2. Provincial Rental Rates

On a provincial level, British Columbia had an average rent of $2,065 per month, edging out Ontario ($2,040) for the highest average rents in September (for all property types).

British Columbia was one of just two provinces to post positive year-over-year rent growth, joining Quebec. Newfoundland ($950) had the lowest average rent in the country. Northwest Territories was the third highest at $1,804 per month, but the sample size of listings is relatively small.

British Columbia and Quebec posted year-over-year increases in average rent of 8% and 14% respectively, while the Northwest Territories was flat. The other provinces in Canada experienced rent deflation, from -1% in Newfoundland and -3% in Alberta, to -13% for Manitoba and Ontario, to -16% for New Brunswick.

British Columbia and Quebec posted year-over-year increases in average rent of 8% and 14% respectively, while the Northwest Territories was flat. The other provinces in Canada experienced rent deflation, from -1% in Newfoundland and -3% in Alberta, to -13% for Manitoba and Ontario, to -16% for New Brunswick.

The average rent levels should not be taken as an apples to apples comparison, as some provinces have higher shares of much larger single-family and townhouse units, while others are dominated by older rental apartments. In Ontario, there is an outsized share of high-rise condominium apartments with new interior finishes, premium views and a wide array of shared amenities.

Provincial Pricing by Property Type

With British Columbia and Quebec seeing rents increase year over year in September, it is important to understand what is driving that growth.

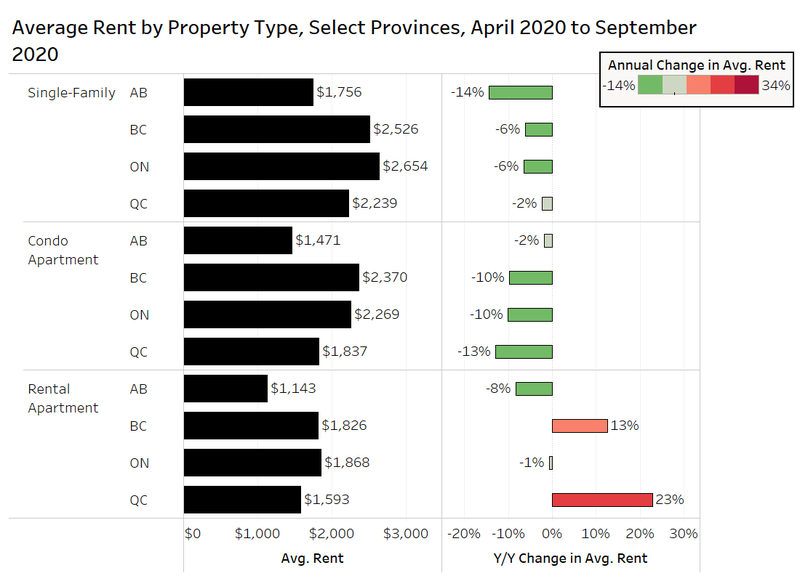

The chart below looks at the average rent for single-family properties, condominium apartments, and rental apartments in Alberta, British Columbia, Ontario, and Quebec during the pandemic period (April to September 2020) compared to the same six month period in 2019.

Average rental rates for single-family homes are down in each of the four provinces, with Alberta seeing the biggest drop at 14%. In terms of condominium apartment rental rates, Alberta is only down 2% annually, but British Columbia, Ontario and Quebec are down by 10% to 13% year over year.

The weakness in the Quebec and British Columbia condo rental markets is in stark contrast to their purpose-built rental markets, which are still experiencing double-digit annual rent growth. The sample sizes in each province are fairly substantial, and it is unlikely that the composition of the listings have a significant impact on average rent levels.

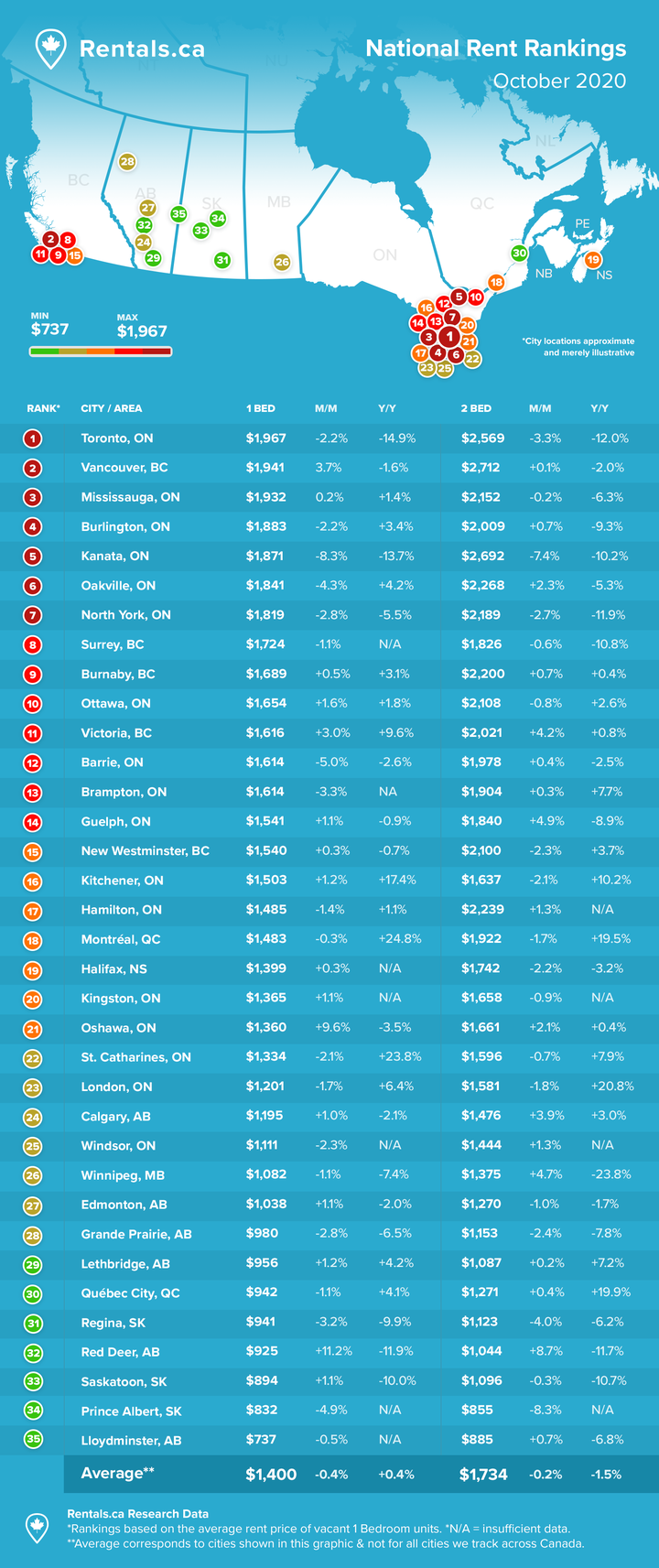

3. Municipal Rental Rates

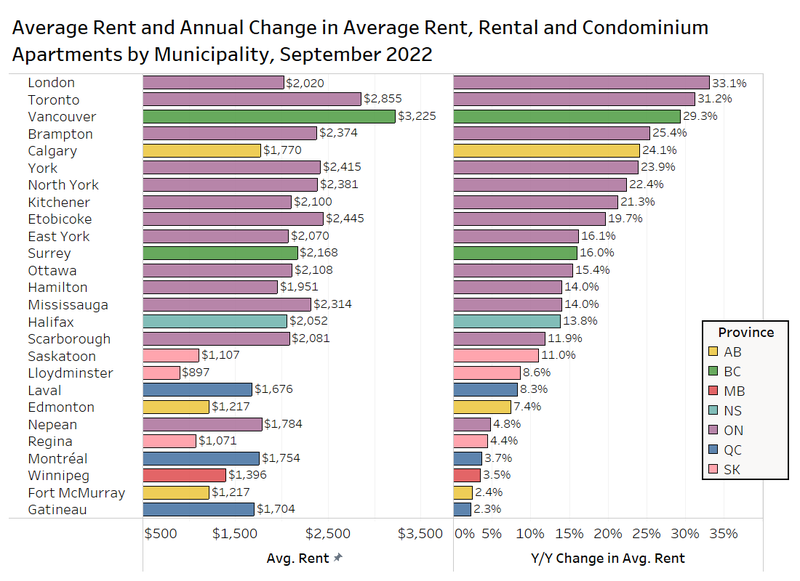

The chart below presents data on the average rental apartment and condominium apartment rental rates by municipality and area in Canada for September 2020, with the annual percent change in average rent shown on the right (includes former municipalities prior to amalgamation in Toronto).

Montreal led all the major municipalities for highest rent appreciation at 17.2% for rental and condo apartments, along with Kitchener at 11.5%. Montreal and Kitchener were the only two major municipalities in all of the country to see positive growth (Hamilton and London were removed from this chart because of a high number of listings from new purpose-built rental apartment projects pulling the average rent up).

Montreal led all the major municipalities for highest rent appreciation at 17.2% for rental and condo apartments, along with Kitchener at 11.5%. Montreal and Kitchener were the only two major municipalities in all of the country to see positive growth (Hamilton and London were removed from this chart because of a high number of listings from new purpose-built rental apartment projects pulling the average rent up).

Two large Ontario municipalities, North York and Toronto, along with Winnipeg, all saw drops in rental rates of about 14%. Toronto’s -14.1% annual rent drop is the worst in the country among major markets.

Vancouver posted the highest average annual rent at $2,249, followed by Toronto at $2,158; Etobicoke next at $2,095; Mississauga at $2,066; and Vaughan at $2,044. North York is the only other municipality showing average annual rents of above $2,000 per month at $2,025.

Municipal Rent Levels by Property Type

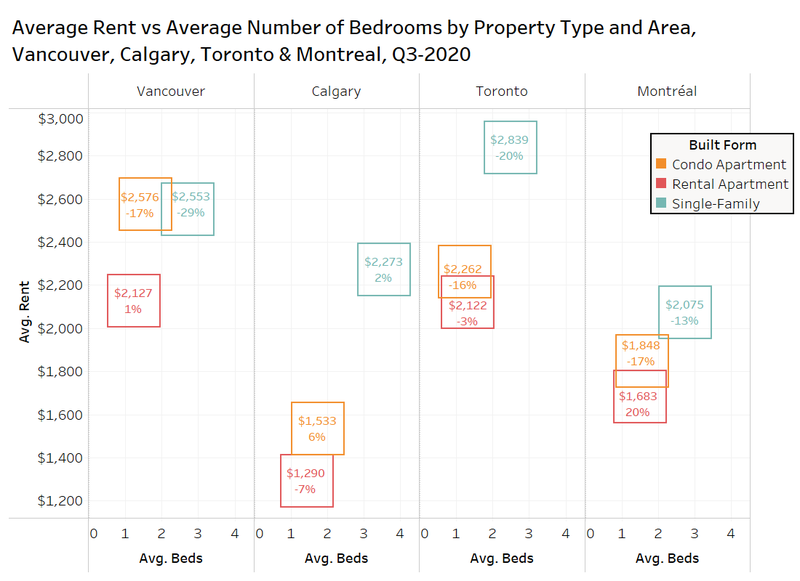

Breaking out the data further by property type and municipality (former municipal boundaries for Toronto) and concentrating on the markets of Vancouver, Calgary, Toronto and Montreal, the chart below shows the average rent on the horizontal axis and the average number of bedrooms on the vertical axis in the third quarter of this year.

In Vancouver, Toronto and Montreal, single-family properties for rent are pretty small at 2.7 bedrooms, 2.5 bedrooms and 2.8 bedrooms, respectively. In Calgary, single-family homes for rent are larger at 3.6 bedrooms on average.

In Vancouver, Toronto and Montreal, single-family properties for rent are pretty small at 2.7 bedrooms, 2.5 bedrooms and 2.8 bedrooms, respectively. In Calgary, single-family homes for rent are larger at 3.6 bedrooms on average.

Despite the earlier rental apartment chart showing higher priced growth for larger properties, the same upward pressure is not being applied to single-detached and semi-detached homes. In Vancouver, the average rent for single-family homes in Q3-2020 was $2,553 per month, lower than condo apartments, and down 29% annually. Condo rents in Vancouver are down 17% in Q3-2020 versus Q3-2019.

In Toronto, single-family rental rates are down 20% year over year in the third quarter, while condo rents are down 16% annually. The average rent for purpose-built apartments is $2,122 per month, down 3% from Q3-2019.

The most bizarre results are occurring in Montreal, with average condo rents down 17% annually, and the average rental apartment rents up 20% annually. It is likely that there are compositional issues here. Changes in the location, unit size, balcony size, level of finish, or unit views can vary significantly from quarter to quarter and impact the rental rates charged by landlords. Secondly, owners of rental apartments are more likely to offer rental incentives like a month or two free rent, that isn’t net out of the Rentals.ca listing data.

4. Ottawa / Rental Rates in Proximity to Canadian Universities

There has been much discussion surrounding the fact that many Canadian universities are conducting classes virtually this fall, and what impact that has on the rental markets in proximity to those areas.

The following charts look at the annual change in rental rates for all property types in London, Edmonton, North York and Toronto close to Western University, The University of Alberta, Ryerson University and University of Toronto, as well as York University.

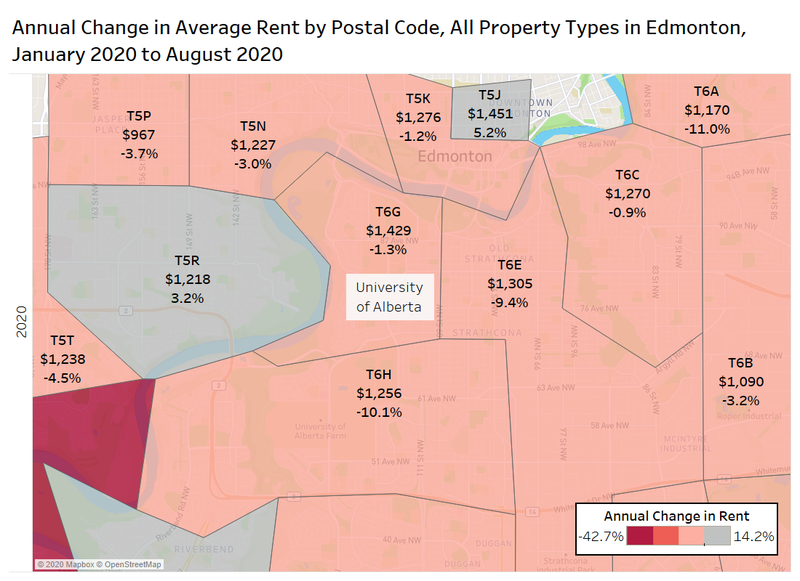

Edmonton

The University of Alberta in Edmonton is in postal code T6G, where the average rent in 2020 (January to September) for all property types was $1,429 per month, a decline of 1.3% from the same period in 2019. The postal codes to the east and south have been hit harder, with annual rent declines of 9.4% in T6E and 10.1% in T6H.

The University of Alberta in Edmonton is in postal code T6G, where the average rent in 2020 (January to September) for all property types was $1,429 per month, a decline of 1.3% from the same period in 2019. The postal codes to the east and south have been hit harder, with annual rent declines of 9.4% in T6E and 10.1% in T6H.

Interestingly, T5G, which is the Edmonton City Centre area downtown has seen average rents increase by 5.2% annually to $1,451 in 2020.

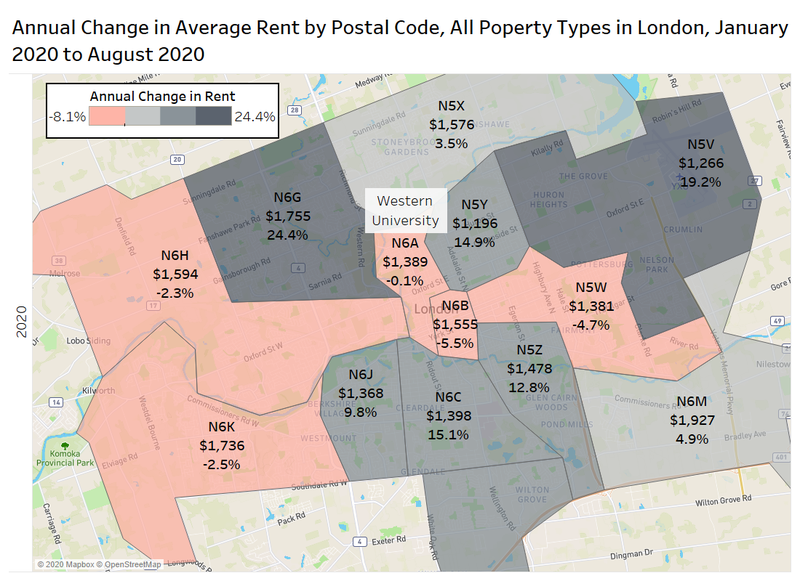

London

London has a strange pattern of rent changes annually, with N6A, where Western University is located, virtually unchanged in 2020 versus 2019 at $1,389 per month.

However, the postal codes to the north of the university have all experienced outsized growth rates with N6G (one of the most active postal codes in terms of listings on Rentals.ca) rising by 24% year over year. Postal code N5Y, just to the east of Western, has increased by nearly 15% annually, but still has a relatively low monthly rent of $1,196 per month.

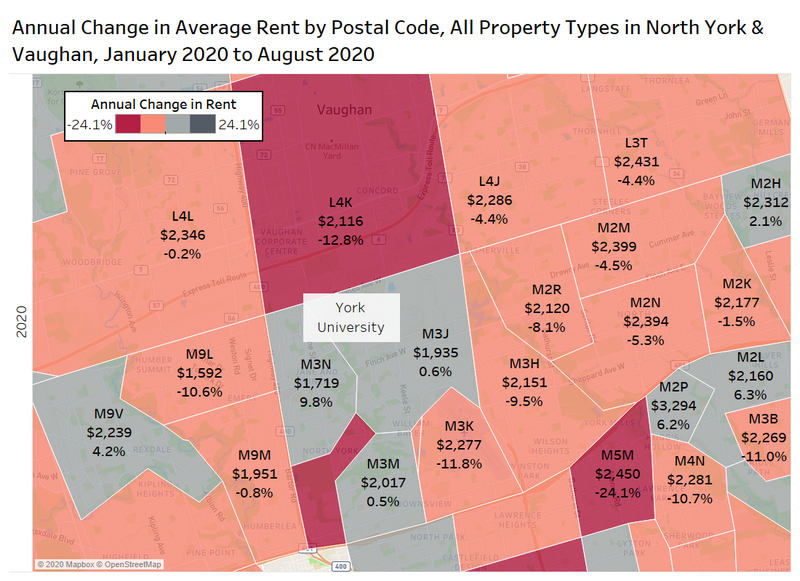

North York / Vaughan

North York / Vaughan

York University is in postal code M3J, where the average rent in 2020 is $1,935 per month for all property types. This rate is actually up year over year by 0.6%.

M3N to the west is up by nearly 10% annually to $1,719 per month, but most of the postal codes surrounding the York University are flat or down significantly.

The most impacted is L4K, which includes the Vaughan Corporate Centre, where the market experienced a decline in average rents of nearly 13% annually to $2,116 per month. The drop might look bad on the surface, as there is a significant number of units under construction in that market and scheduled for completion over the next 18 months. But there were two major completions in 2020 — Met Condos and Nord Condos — and these two buildings contain a high number of small suites, so the average rent per square foot actually increased by 28% annually, despite the drop in the monthly rent.

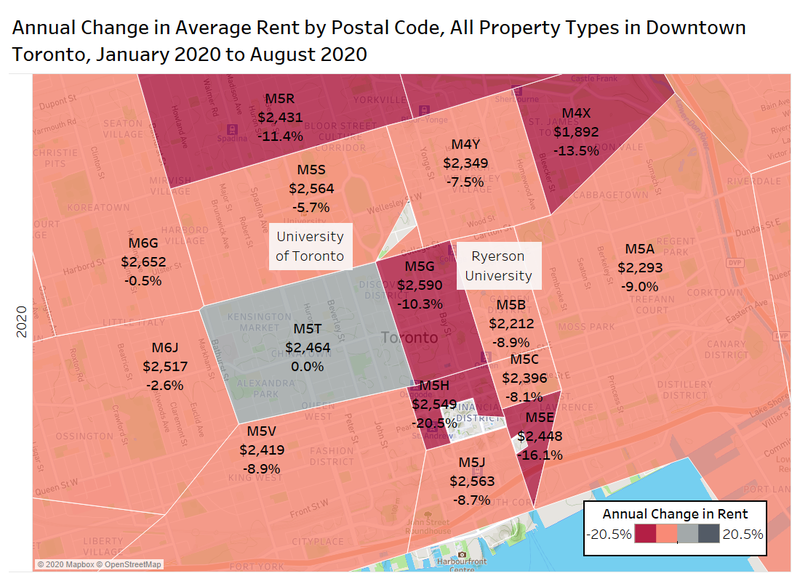

Downtown Toronto

Downtown Toronto

There has been much discussion surrounding the drop in rents downtown due to the shutdown of many of the office towers, and a reduction in demand for short-term rentals from tourist and out-of-town contract workers. With Ryerson and U of T downtown, as well as several other colleges, many students decided to stay with their parents, or move back with their parents to save money and learn virtually.

The average rent in M5B where Ryerson University is has declined by about 9% annually to $2,212 per month, while M5S, where the University of Toronto is, has seen average rents decline by 5.7% annually to $2,564 per month. The only area of downtown Toronto to not experience a decline in rent was M5T, which was flat year over year at $2,464 per month. However, on a rent per-square-foot basis, M5T has declined by 2% annually.

5. Downtown Toronto Investor Condos

The decline in average rent downtown can be attributed to the high number of condos for rent. Demand has dropped off due to COVID-19, and there is a significant influx of new supply hitting the market via completed projects.

In downtown Toronto, condominium apartments often take two to four years to build given their size and complexity, so there is about a four-year lag between the sales and occupancy of these projects. In 2016 and 2017, the Toronto new condominium apartment market set record highs for sales, and those buildings are coming to completion now. A high share of those units were purchased by investors with the intent of renting them out to young professionals.

The chart below looks at a selection of condominium apartments completed between 2015 and 2019 in Toronto with at least 20 listings in April to September 2019 AND 20 or more listings in the pandemic-impacted period of April 2020 to September 2020. The average rent per square foot, annual change in listings, and annual change in average rent per square foot are shown.

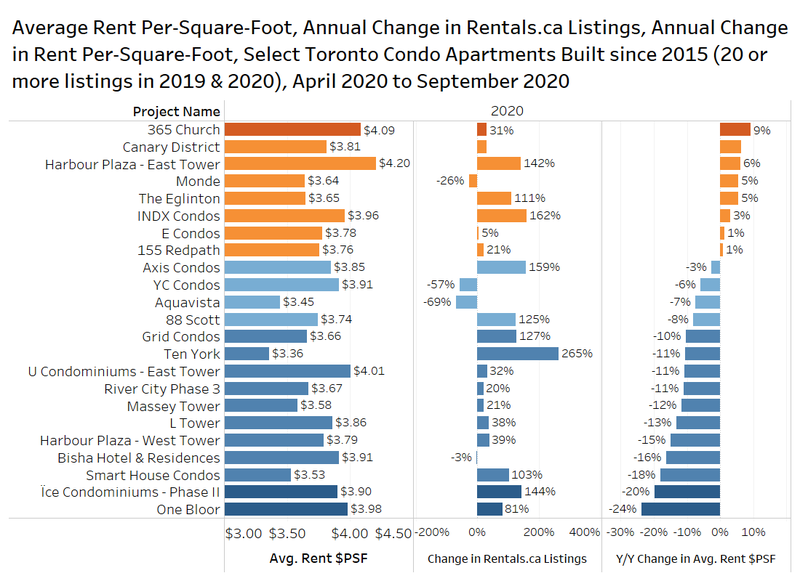

Of the 23 projects on the list, 15 experienced a decline in their average rent per square foot, with the largest decline at One Bloor, the 76-storey tower at the corner of Yonge and Bloor, with a 24% decline year over year to $3.98 per square foot. Listings on Rentals.ca for this project increased by 81% annually.

Of the 23 projects on the list, 15 experienced a decline in their average rent per square foot, with the largest decline at One Bloor, the 76-storey tower at the corner of Yonge and Bloor, with a 24% decline year over year to $3.98 per square foot. Listings on Rentals.ca for this project increased by 81% annually.

Ten York, in Toronto’s south core area, has experienced an increase in listings of 265% on Rentals.ca in 2020, and rents on a per-foot basis have declined by 11%.

The data suggests there might not be an urban exodus in Toronto’s Village neighbourhood, as 365 Church has experienced a 9% increase in rent per square foot in April to September 2020 compared to the same period last year. The $4.09 per square foot is the second highest among the 23 projects on the chart.

However, it should be kept in mind these are asking rents, and can be skewed by a few landlords that refuse to accept the new reality that rents have declined in most parts of the city. Secondly, there are always compositional issues with listing samples, as there could be large penthouses with upgraded features in one period and less desirable lower-level units with no balconies in the next period.

6. Conclusion

The rental market on a national basis continues to tread water, with the average rent staying flat at about $1,770 per month over the last four months.

The data on a national basis suggests that tenants are looking for larger units, either by square footage or by number of bedrooms, but appear to be avoiding the most expensive single-family properties and condominium apartments in prime neighbourhoods.

The work-from-home phenomenon and pandemic continue to shift demand patterns as tenants look at different locations farther from their place of employment, cheaper properties, and units with more space.

The latest employment data suggests Canada added nearly 380,000 jobs in September, and analysts have estimated that 75% of employees who lost their jobs during the early months of the pandemic have been rehired or found new work.

With schools open and day cares re-opening, and the paring back of government assistance programs, more Canadians have the ability and motivation to return to work, and/or look for work. More employed Canadians and more hiring results in more demand for housing, and could send the rental trendline climbing upward again this winter.

Rentals.ca Data

The data used in this analysis is based on monthly listings from Rentals.ca. The data is much different than the more familiar numbers collected and published by Canada Mortgage Housing Corporation (CMHC).

Rentals.ca data includes basement apartments, rental apartments, condominium apartments, townhouses, semi-detached houses and single-detached houses, where CMHC’s primary rental data only includes rental apartments and rental townhouses. CMHC collects some data on the secondary market, but it is reported separately.

The CMHC rental rates are based on the entire universe of purpose-built rental units in Canada (the stock), while Rentals.ca data is primarily based on the asking rents of vacated units only (the flow) — this is a smaller sample size, but more representative of the actual market rent a prospective tenant encounters. The Rentals.ca data set typically produces much higher rental rates in comparison to CMHC, as vacated units are not subject to rent control.

The average and median rental rates via Rentals.ca can also skew higher than CMHC’s data for several reasons: The inclusion of larger and more expensive unit types like singles, row units and condos; the survivorship bias (overpriced units remain in the sample longer); and the multiple listings of the same property at different rent levels every month.

It should also be noted that properties listed for above $5,000 a month and below $500 a month are eliminated from the sample of units analyzed. Also, short-term leases, single-room rentals, and furnished rental units are eliminated from the sample where identifiable.

Rentals.ca is Canada’s premier online marketplace for renters and landlords, providing a comprehensive suite of tools and resources tailored to simplify the rental process. With an extensive selection of listings across the country, Rentals.ca offers user-friendly search functionality that helps renters find their perfect home efficiently. For landlords, Rentals.ca delivers effective advertising solutions to maximize visibility and fill vacancies faster. Committed to innovation and excellence, Rentals.ca aims to empower users with up-to-date market insights and expert guidance, making renting easier and more accessible for everyone.