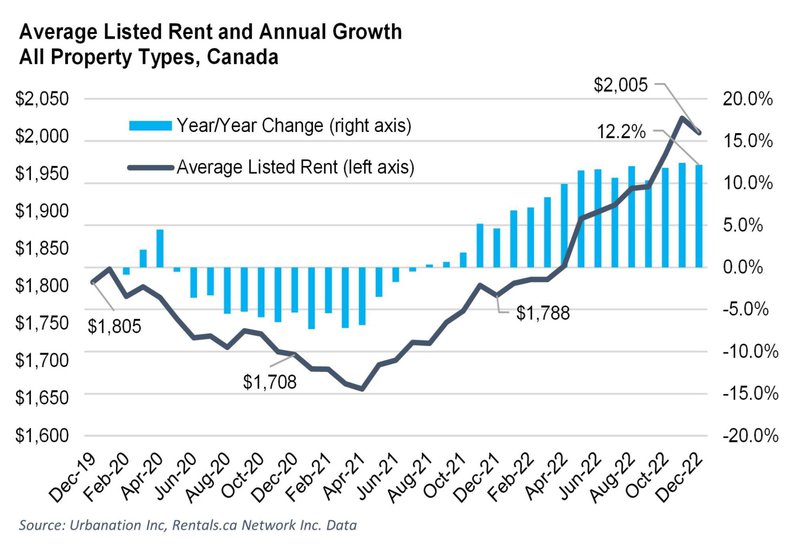

The annual rate of rent inflation in Canada remained in double-digits for the eighth consecutive month in December. The average listed rent for all property types increased 12.2% year over year to reach $2,005, an increase of $217 from the December 2021 average of $1,788. On a month-over-month basis, average rents decreased 1.0%, which is a typical seasonal occurrence. This is the second straight month the average monthly rent has exceeded $2,000.

Rentals.ca January 2022 Rent Report

Rentals.ca January 2022 Rent Report

1. National Overview

Average Rent Increase in Canada during 2022 was 11%

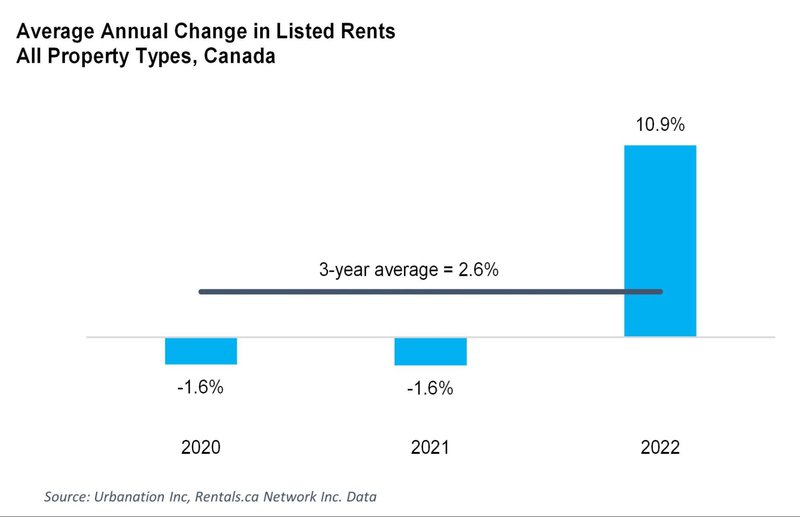

The average rate of annual rent increase for 2022 as a whole was 10.9%, which followed 1.6% average annual rent declines recorded for both 2021 and 2020, resulting in a three-year average rent increase of 2.6% — below the general rate of inflation in the economy over the same time period[1].

The exceptional growth in rents last year can be attributed to a combination of factors, including a recovery from declines experienced during the pandemic, record high population growth, a large pullback in home buying, and structurally low vacancy rates. Of note, the strong growth in rents occurred in 2022 despite a record high for total apartment completions last year.

[1] Reported rent increases only reflect units that turned over in the market. The majority of rental units do not have an annual change in tenancy and are subject to provincial rent increase guidelines.

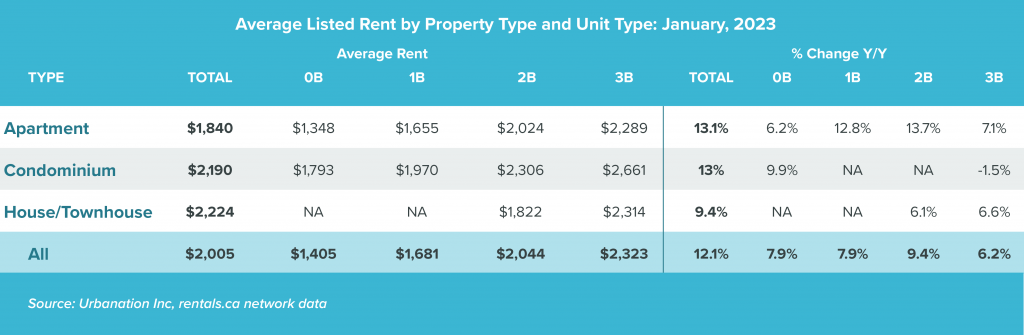

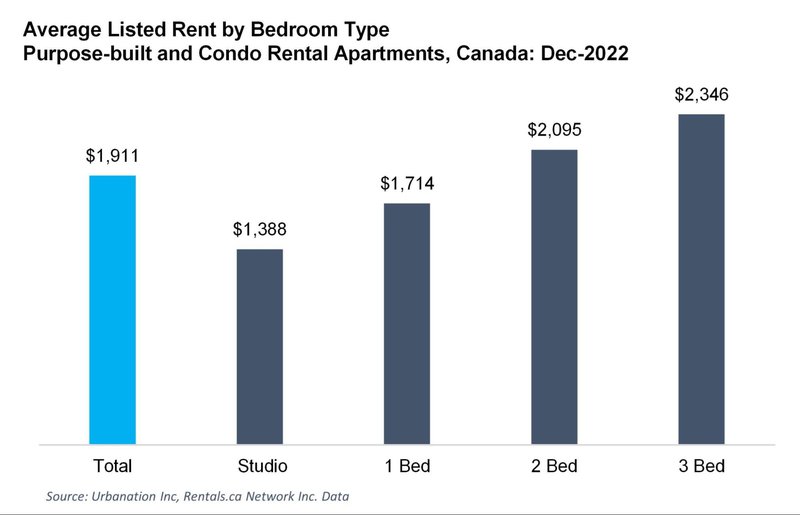

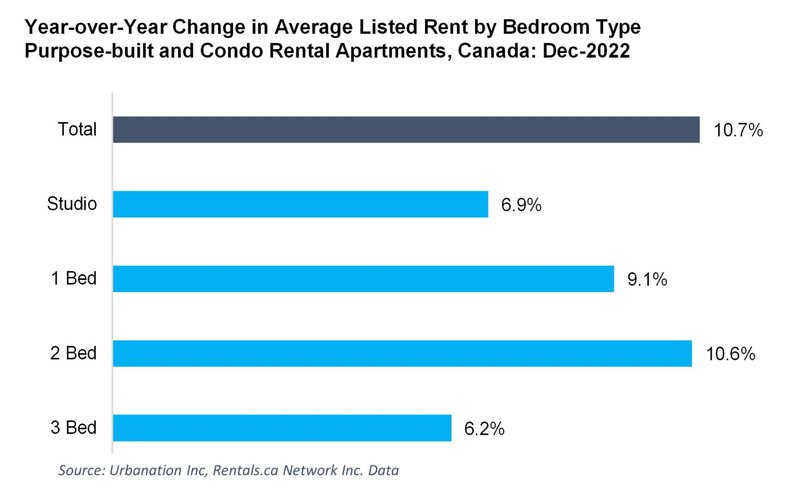

Combined rents for purpose-built and condominium apartment rentals increased 10.7% annually to an average of $1,911. Consistent with previous months, annual rent growth was strongest for two-bedroom units at 10.6%, reaching an average of $2,095. One-bedroom rents averaged $1,714 and increased 9.1% annually, while studios increased 6.9% from a year earlier to an average of $1,368. The slowest rate of rent increase was for three-bedroom units at 6.2%, rising to an average of $2,346.

2. Provincial Overview

*Totals are reflective of all available listings and not the data listed within individual tables

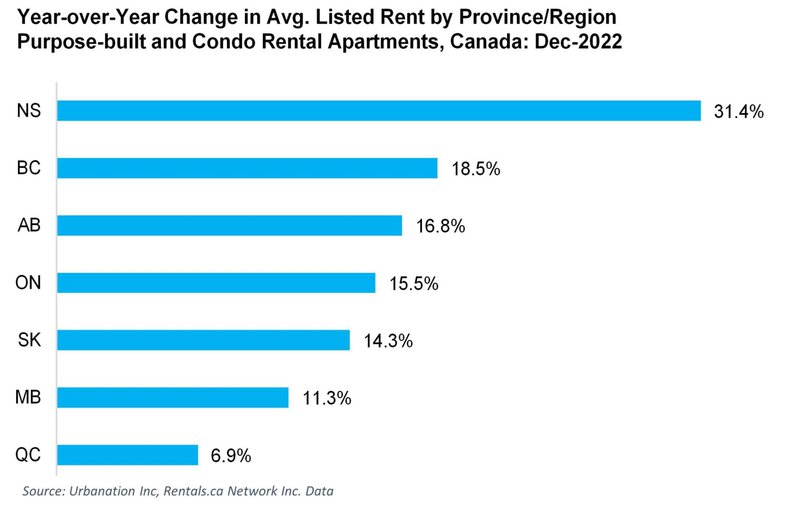

Provincial Rent Growth Connected to Population Growth

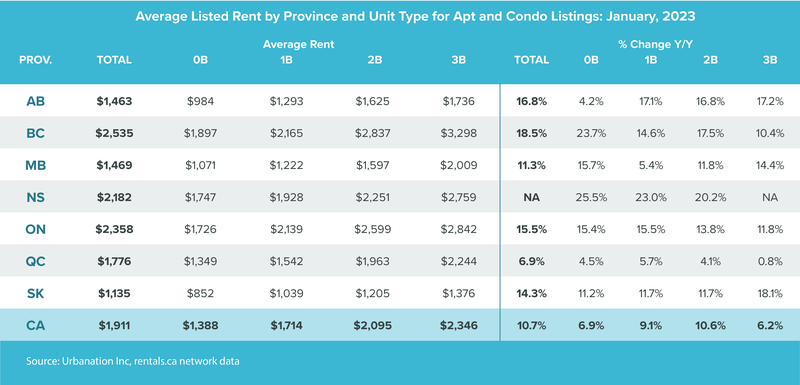

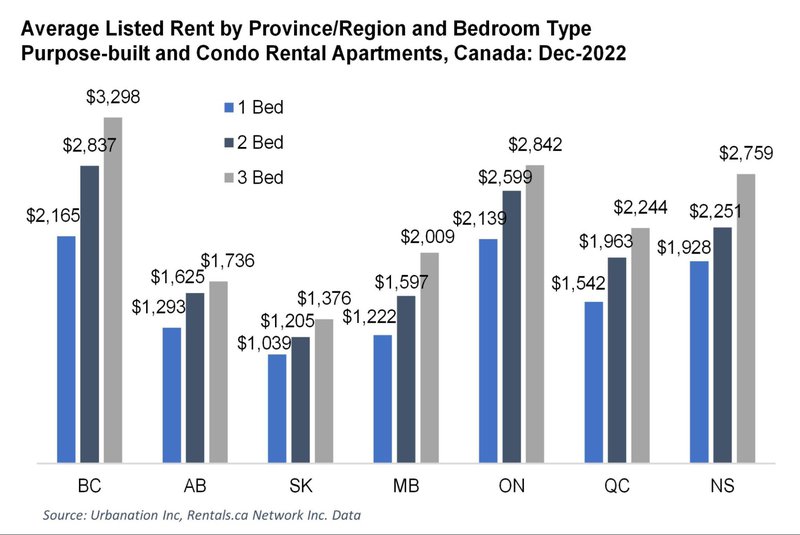

Provincially, rent growth correlated with population growth. Nova Scotia, along with other Atlantic provinces, had the fastest growing populations in 2022, boosting average rents for apartments up 31% year over year in December to an average of $2,182. Outside of Atlantic Canada, the fastest population growth occurred in British Columbia and Alberta, posting the second and third fastest rates of annual rent increases in December of 18.5% and 16.8%, respectively, to $2,535 (BC) and $1,463 (AB). Ontario posted above-average population growth and rent growth in 2022, with December rents up 15.5% annually to $2,358. The slowest growing province for both population and rents in 2022 was Quebec, which recorded a 6.9% annual rent increase in December 2022 to an average of $1,776.

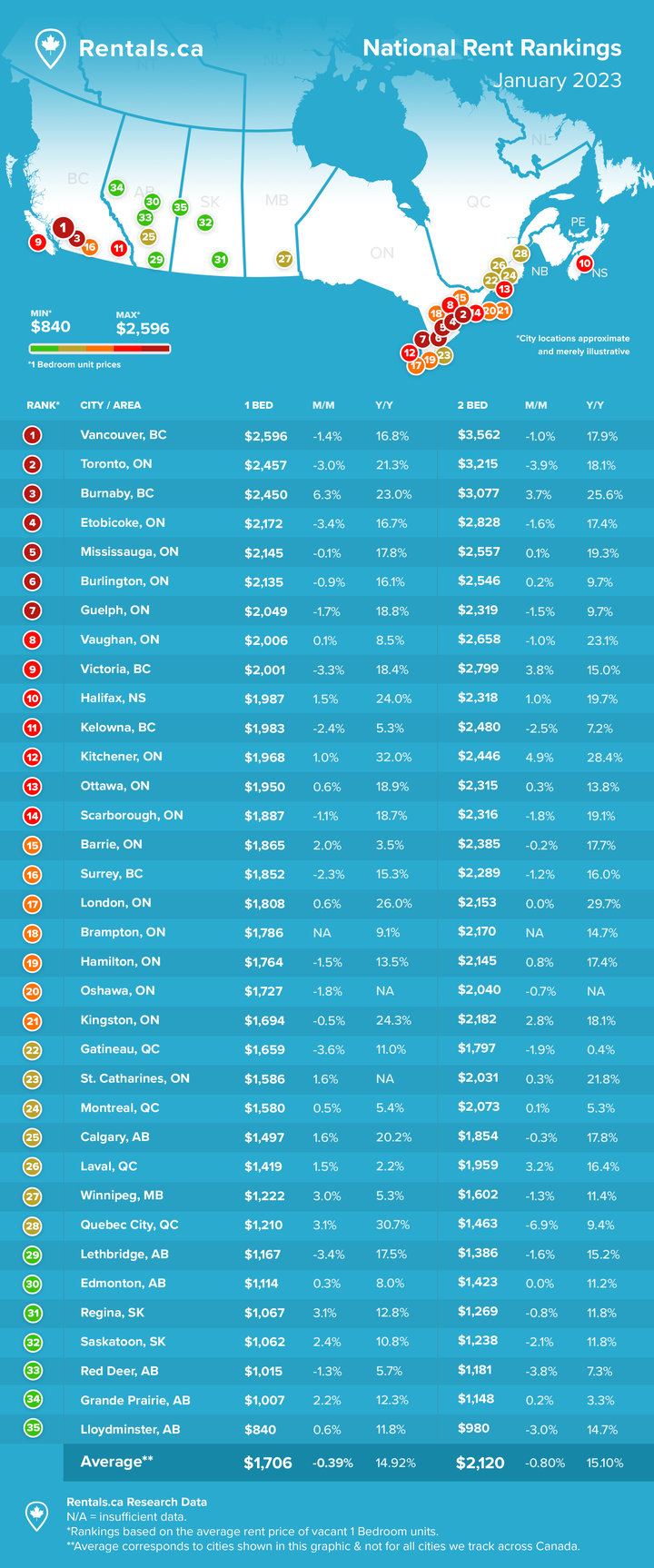

3. Municipal Rental Rates

*Totals are reflective of all available listings and not the data listed within individual tables

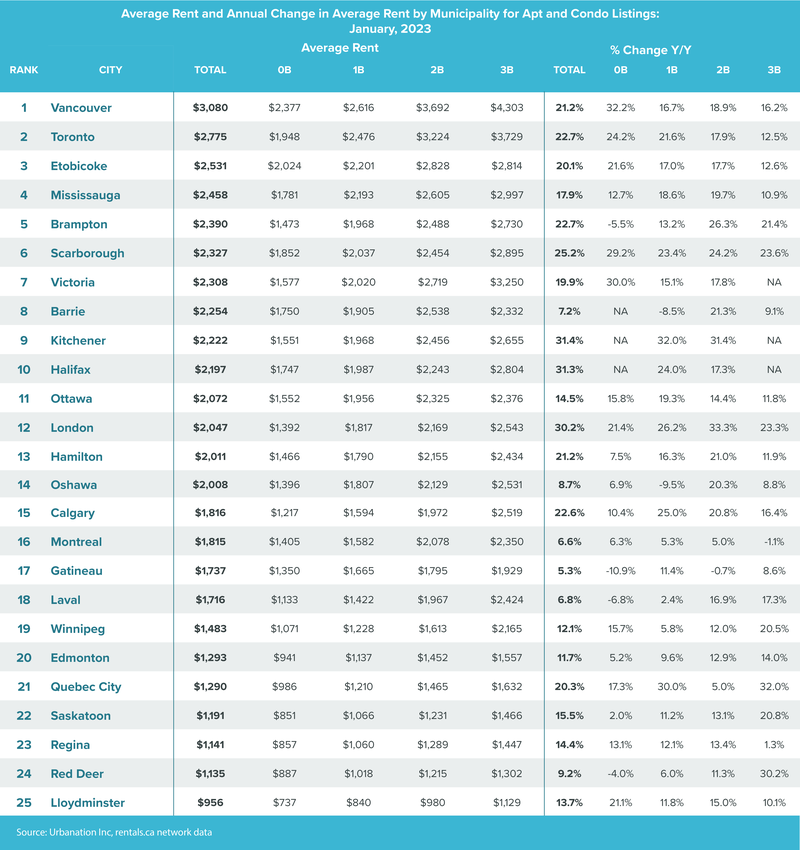

Rents Accelerating Quickly in Calgary

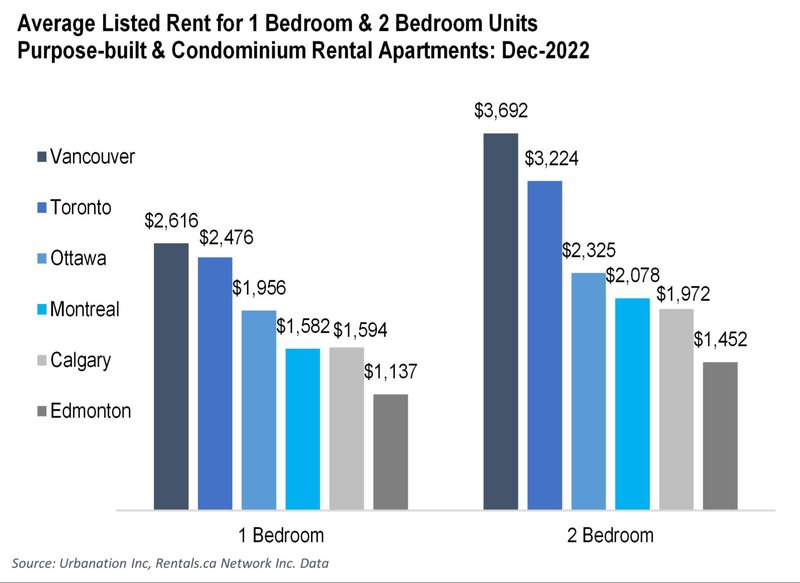

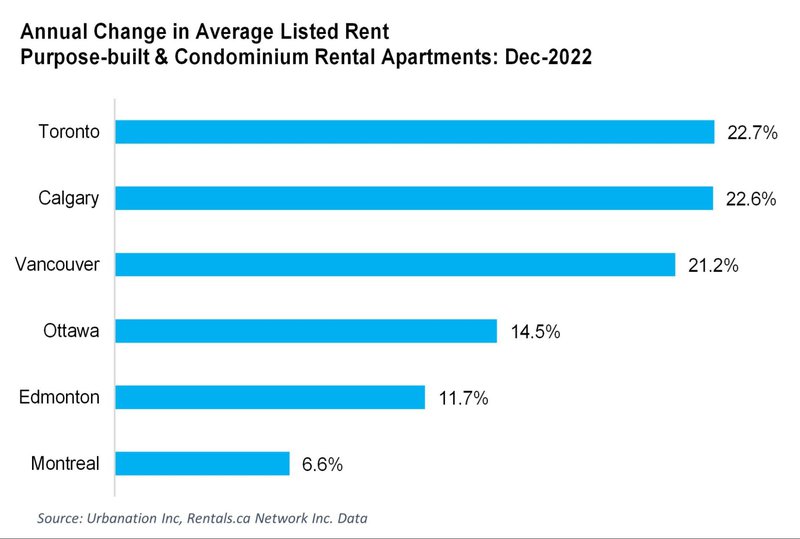

Annual rent increases for apartments remained strong in the most expensive markets in Toronto and Vancouver, posting 22.7% and 21.2% growth, respectively, pushing average rents in December to $2,775 and $3,080. Strong economic momentum in Calgary has led to a quick acceleration in rents, which elevated the city into the second spot for rent growth in December with a 22.6% increase to an average of $1,816. The Ottawa and Edmonton markets ranked fourth and fifth for rent growth in December with annual increases of 14.5% and 11.7%, respectively, with the slowest growing market amongst Canada’s largest cities represented by Montreal with 6.6% annual growth.

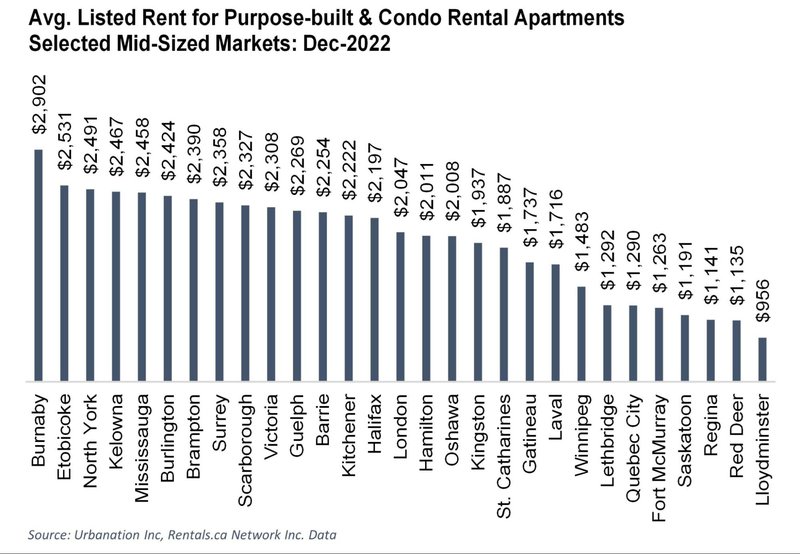

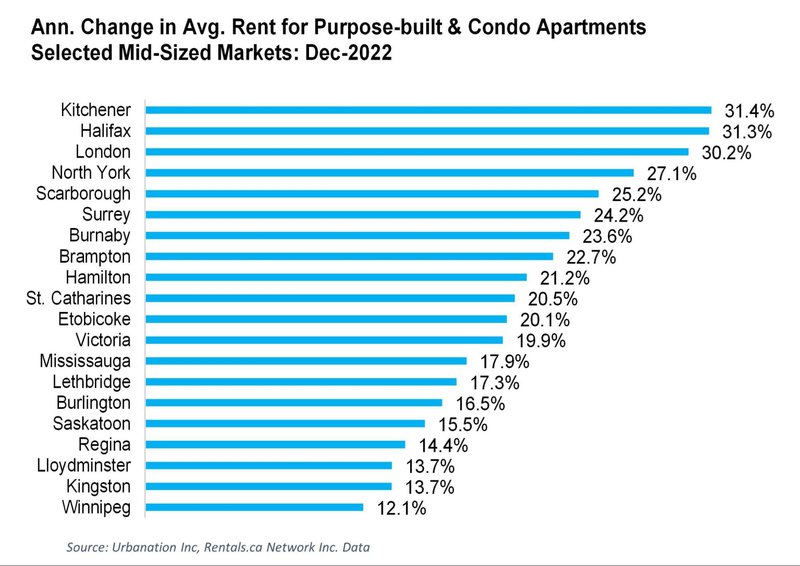

Kitchener, Halifax and London Post 30% Annual Growth in December

Among medium-sized markets, annual rent increases of over 30% in December were recorded in cities that experienced some of the fastest rates of population growth in 2022, including Kitchener, Halifax and London. Also ranking high on the list for annual rent growth in December were markets that border Toronto and Vancouver, including North York, Scarborough, Surrey and Burnaby — posting annual increases of between 23.6% and 27.1%. Fast annual rent growth was also concentrated in markets positioned southwest of Toronto, which included Hamilton (21.2%), St. Catharines (20.5%), Etobicoke (20.1%), Mississauga (17.9%), and Burlington (16.5%). Within British Columbia and Ontario, above-average annual rent growth in December was also identified in Kingston (13.7%) and Victoria (19.9%), while Alberta rents increased quickly in Lethbridge (17.3%) and Lloydminster (13.7%), as well as other prairie markets including Saskatoon (15.5%), Regina (14.4%), and Winnipeg (12.1%).

4. 2023 Rental Market Outlook

2023 Rental Market Outlook

The Canadian rental market is carrying strong momentum into 2023, driven by robust labour market conditions, record high population inflows, and generational lows for homeownership affordability.

While the rental sector is projected to remain in an expansionary mode this year as demand factors remain supportive, more moderate rates of rent growth can be expected as the economy and employment begin to soften following the rapid rise in interest rates and as renters face affordability constraints after rents surged to record highs last year. Ongoing strength in population growth and suppressed first-time home buying activity will be supportive of the rental market this year, although a more than 40-year high anticipated for rental completions in 2023 will help to temper further rent increases.

It is expected that rents for units available in the market will increase by an average of about 5% in Canada during 2023, which is more aligned with current rates of income growth and the long-term historical average for rent inflation.

Markets in Canada experiencing high rates of population growth, low vacancy and relatively modest amounts of new rental construction should drive rent inflation in 2023. Atlantic Canada can be expected to continue leading the country in rent growth, with ongoing strength anticipated in Ontario and British Columbia. Alberta rents are also showing strong upside potential, while Quebec rent growth is likely to continue trailing the national average.

Rentals.ca Data

The data used in this analysis is based on monthly listings from the Rentals.ca Network of Internet Listings Services (ILS). This data differs from the numbers collected and published by the Canada Mortgage Housing Corporation (CMHC).

The Rentals.ca Network of ILS’s data covers both the primary and secondary rental markets and includes basement apartments, rental apartments, condominium apartments, townhouses, semi-detached houses, and single-detached houses. CMHC’s primary rental data only includes purpose-built rental apartments and rental townhouses. CMHC also collects data on secondary market rentals, but this is reported separately.

CMHC’s rental rates are based on the entire universe of purpose-built rental units (rental stock), regardless of rental tenure. CMHC rental rates are reflective of what the average household spends on rental housing and not the current market rents for vacant units. The data used in this report is based on the asking rates of available (vacant) units only and reflect on-going trends in the market. This covers a smaller sample size but is more representative of the actual market rent a prospective tenant would encounter. The Rentals.ca Network of ILS’s data typically provides much higher rental rates compared to CMHC, as vacant units typically reset to market rates when not subject to rent control.

The average and median rental rates in this report can also skew higher than CMHC’s data for the following reasons: the inclusion of larger more expensive unit types such as single-family homes, townhouse units, and large luxury condominium units; the presence of duplicate or multiple listings at the same property and the survivorship bias where more expensive or over-priced units take longer to lease and remain in the sample longer.

Properties listed for greater than $5,000 per month, and less than $500 per month are removed from the sample. Similarly, short-term rentals, single-room rentals, and furnished suites are removed from the sample when identifiable.

Urbanation is a real estate research firm providing market research.

Urbanation provides in-depth market analysis and consulting services to the apartment industry since 1981. Urbanation uses a multi-disciplinary approach that combines empirical research techniques, industry relationships forged over the past four decades, and first-hand observations and site visitations. Urbanation offers subscription services and custom market feasibility studies covering the new construction condominium and purpose-built rental apartment markets in Ontario.